Bitcoin – the virtual banking currency of the internet – has existed for several years now and many people have questions about them. Where do they come from? Are they legal? Where can you get them? We've got the answers to those questions and more.

What Are Bitcoins?

Bitcoins are electronic currency, otherwise known as 'cryptocurrency'. Bitcoins are a form of digital public money that is created by painstaking mathematical computations and policed by millions of computer users called 'miners'.

Bitcoins are, in essence, electricity converted into long strings of code that have money value.

Why Bitcoins Are So Controversial

Various reasons have converged to make Bitcoin currency a real media sensation.

From 2011-2013, criminal traders made bitcoins famous by buying them in batches of millions of dollars so they could move money outside of the eyes of law enforcement. Subsequently, the value of bitcoins skyrocketed.

Ultimately, though, bitcoins are highly controversial because they take the power of making money away from central federal banks, and give it to the general public. Bitcoin accounts cannot be frozen or examined by tax men, and middleman banks are completely unnecessary for bitcoins to move. Law enforcement and bankers see bitcoins as 'gold nuggets in the wild wild west', beyond the control of traditional police and financial institutions.

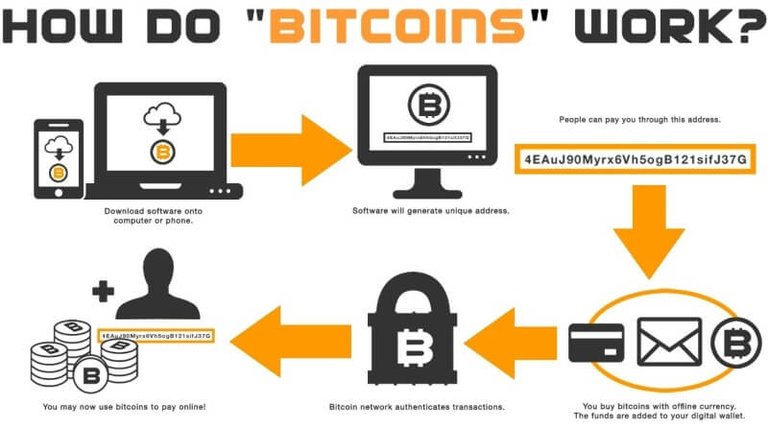

How Bitcoins Work

Bitcoins are completely virtual coins designed to be 'self-contained' for their value, with no need for banks to move and store the money.

Once you own bitcoins, they behave like physical gold coins: they possess value and trade just as if they were nuggets of gold in your pocket. You can use your bitcoins to purchase goods and services online, or you can tuck them away and hope that their value increases over the years.

Bitcoins are traded from one personal 'wallet' to another.

A wallet is a small personal database that you store on your computer drive, on your smartphone, on your tablet, or somewhere in the cloud.

For all intents, bitcoins are forgery-resistant. It is so computationally-intensive to create a bitcoin, it isn't financially worth it for counterfeiters to manipulate the system.

Bitcoin Values and Regulations

A single bitcoin varies in value daily; you can check places like Coindesk to see today's value. There are more than two billion dollars worth of bitcoins in existence. Bitcoins will stop being created when the total number reaches 21 billion coins, which will be sometime around the year 2040. As of 2017, more than half of those bitcoins had been created.

Bitcoin currency is completely unregulated and completely decentralized. There is no national bank or national mint, and there is no depositor insurance coverage. The currency itself is self-contained and un-collateraled, meaning that there is no precious metal behind the bitcoins; the value of each bitcoin resides within each bitcoin itself.

Bitcoins are stewarded by 'miners', the massive network of people who contribute their personal computers to the Bitcoin network. Miners act as a swarm of ledger keepers and auditors for Bitcoin transactions.

Miners are paid for their accounting work by earning new bitcoins for each week they contribute to the network.

How Bitcoins Are Made

A bitcoin, at its core, is a very simple data ledger file called a 'blockchain'. A blockchain's file size is quite small, similar to the size of a long text message on your smartphone.

Each bitcoin blockchain has three parts, two of which are very simple: its identifying address (of approximately 34 characters), and the history of who has bought and sold it (the ledger).

The complex part of the bitcoin is its third part: the private key header log. This header is where a sophisticated digital signature is captured to confirm each and every transaction for that particular bitcoin file.

Each digital signature is unique to each individual user and his/her personal bitcoin wallet.

These signature keys are the security system of bitcoins: Every single trade of bitcoin blockchains is tracked and tagged and publicly disclosed, with each participant's digital signature attached to the bitcoin blockchain as a 'confirmation'. These digital signatures, when given several seconds to confirm their transactions across the network, prevent transactions from being duplicated and people from forging bitcoins.

Note: While every bitcoin records the digital address of every bitcoin wallet it touches, the bitcoin system does NOT record the names of the individuals who own wallets. In practical terms, this means that every bitcoin transaction is digitally confirmed but is completely anonymous at the same time.

Your bitcoins are stored on a computer device of your choice, but the history of each bitcoin you own or spend is publicly stored on the bitcoin network, and every user will be able to see every bitcoin's history.

While people cannot easily see your personal identity, people can see the history of your bitcoin wallet. This is a good thing, as a public history adds transparency and security, helps deter people from using bitcoins for dubious or illegal purposes.

You can see bitcoin transactions at blockchain.info. These are public ledgers of all the bitcoin wallets on the planet. Note: There are no people's names attached; the wallets themselves are completely anonymous.

Banking or Other Fees to Use Bitcoins

There are very small fees to use bitcoins. However, there are no ongoing banking fees with bitcoin and other cryptocurrency because there are no banks involved. Instead, you will pay small fees to three groups of bitcoin services: the servers (nodes) who support the network of miners, the online exchanges that convert your bitcoins into dollars, and the mining pools you join.

The owners of some server nodes will charge one-time transaction fees of a few cents every time you send money across their nodes, and online exchanges will similarly charge when you cash your bitcoins in for dollars or euros. Additionally, most mining pools will either charge a small one percent support fee or ask for a small donation from the people who join their pools.

In the end, while there are nominal costs to use Bitcoin, the transaction fees and mining pool donations are much cheaper than conventional banking or wire transfer fees.

Bitcoin Production Facts

Bitcoins can be 'minted' by anyone in the general public who has a strong computer. Bitcoins are made through a very interesting self-limiting system called cryptocurrency mining and the people who mine these coins are called miners. It is self-limiting because only 21 million total bitcoins will ever be allowed to exist, with approximately 11 million of those Bitcoins already mined and in current circulation.

Bitcoin mining involves commanding your home computer to work around the clock to solve 'proof-of-work' problems (computationally-intensive math problems). Each bitcoin math problem has a set of possible 64-digit solutions. Your desktop computer, if it works nonstop, might be able to solve one bitcoin problem in two to three days, likely longer.

For a single personal computer mining bitcoins, you may earn perhaps 50 cents to 75 cents USD per day, minus your electricity costs.

For a very large-scale miner who runs 36 powerful computers simultaneously, that person can earn up to $500 USD per day, after costs.

Indeed, if you are a small-scale miner with a single consumer-grade computer, you will likely spend more in electricity that you will earn mining bitcoins. Bitcoin mining is only really profitable if you run multiple computers, and join a group of miners to combine your hardware power. This very prohibitive hardware requirement is one of the biggest security measures that deters people from trying to manipulate the Bitcoin system.

Bitcoin Security

They are as secure as possessing physical precious metal. Just like holding a bag of gold coins, a person who takes reasonable precautions will be safe from having their personal cache stolen by hackers.

Your bitcoin wallet can be stored online (i.e. a cloud service) or offline (a hard drive or USB stick). The offline method is more hacker-resistant and absolutely recommended for anyone who owns more than 1 or 2 bitcoins.

More than hacker intrusion, the real loss risk with bitcoins revolves around not backing up your wallet with a failsafe copy. There is an important .dat file that is updated every time you receive or send bitcoins, so this .dat file should be copied and stored as a duplicate backup every day you do bitcoin transactions.

Security note: The collapse of the Mt.Gox bitcoin exchange service is not due to any weakness in the Bitcoin system. Rather, that organization collapsed because of mismanagement and their unwillingness to invest any money in security measures. Mt.Gox, for all intents and purposes, had a large bank with no security guards, and it paid the price.

Abuse of Bitcoins

There are currently three known ways that bitcoin currency can be abused.

- Technical weakness – time delay in confirmation: bitcoins can be double-spent in some rare instances during the confirmation interval. Because bitcoins travel peer-to-peer, it takes several seconds for a transaction to be confirmed across the P2P swarm of computers. During these few seconds, a dishonest person who employs fast clicking can submit a second payment of the same bitcoins to a different recipient.

While the system will eventually catch the double-spending and negate the dishonest second transaction, if the second recipient transfers goods to the dishonest buyer before they receive confirmation, then that second recipient will lose both the payment and the goods.

Human dishonesty – pool organizers taking unfair share slices: Because bitcoin mining is best achieved through pooling (joining a group of thousands of other miners), the organizers of each pool get the privilege of choosing how to divide up any bitcoins that are discovered. Bitcoin mining pool organizers can dishonestly take more bitcoin mining shares for themselves.

Human mismanagement – online exchanges: With Mt. Gox being the biggest example, the people running unregulated online exchanges that trade cash for bitcoins can be dishonest or incompetent. This is the same as Fannie Mae and Freddie Mac investment banks going under because of human dishonesty and incompetence. The only difference is that conventional banking losses are partially insured for the bank users, while bitcoin exchanges have no insurance coverage for users.

Four Reasons Why Bitcoins Are Such a Big Deal

There is a lot of controversy around bitcoins. These are the top reasons why:

- Bitcoins are not created by any central bank, nor regulated by any government. Accordingly, there are no banks logging your money movement, and government tax agencies and police cannot track your money. This is bound to change eventually, as unregulated money is a real threat to government control, taxation, and policing.

Indeed, bitcoins have become a tool for contraband trade and money laundering, precisely because of the lack of government oversight. The value of bitcoins skyrocketed in the past because wealthy criminals were purchasing bitcoins in large volumes.

- Bitcoins completely bypass banks. Bitcoins are transferred via a peer-to-peer network between individuals, with no middleman bank to take a slice.

Bitcoin wallets cannot be seized or frozen or audited by banks and law enforcement. Bitcoin wallets cannot have spending and withdrawal limits imposed on them. For all intents: nobody but the owner of the bitcoin wallet decides how their wealth will be managed.

This is really threatening to banks, as you might guess.

- Bitcoins are changing how we store and spend our personal wealth. Since the advent of printed (and eventually virtual) money, the world has handed over the power of currency to a central mint and various banks. These banks print our virtual money, store our virtual money, move our virtual money, and charge us for their middleman services.

If banks need more currency, they simply print more or conjure more digits in their electronic ledgers. This system is easily abused and gamed by banks because paper money is essentially paper checks with a promise to have value, with no actual physical gold behind the scenes to back those promises.

Bitcoins are designed to put the control of personal wealth back into the hands of the individual. Instead of paper or virtual bank balances that promise to have value, Bitcoins are actual packages of complex data that have value in themselves.

- Bitcoin transactions are irreversible. Conventional payment methods, like a credit card charge, bank draft, personal checks, or wire transfer, do have the benefit of being insured and reversible by the banks involved. In the case of bitcoins, every time bitcoins change hands and change wallets, the result is final. Simultaneously, there is no insurance protection of your bitcoin wallet: If you lose your wallet's hard drive data or even your wallet password, then your wallet's contents are gone forever.

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://www.lifewire.com/what-are-bitcoins-2483146

Congratulations @steepupvotrx! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOPCongratulations @steepupvotrx! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOP