Bitcoins and crypto trading are the new age investment attractions in India, rather many exchanges have cropped up in the last 6 months giving access; especially retail traders to invest in crypto currencies. These are privately run websites, calling themselves crypto exchanges & offering various virtual / crypto currencies, which are yet unregulated by the government, however such exchanges are either self governed or run on industry accepted principles of trade, KYCs and public deposit rules.

The recent surge in valuations of virtual currencies and resultant unprecedented gains made by traders have attracted attention of the Tax Officers to the world of crypto currencies and thereby the taxation of it.

Though the Union Government has entrusted the Department of Economic Affairs (DEA), Ministry of Finance (MoF) under the control of Finance Minister, Sh. Arun Jaitley, to formulate a framework for regulation of crypto currencies in India. (In this regard, Sh. Subash Chandra Garg, Secretary of DEA, MoF, Govt of India, as reported, has been given responsibility for drafting the regulatory framework for virtual currencies), there are also expectations that the Union Budget 2018 shall either define or deny, thereby clearing stance of the government, on legality of crypto currencies in India.

While the crypto currency community awaits with bated breath for the regulatory framework by the government, there has been an unconfirmed Tax Notice going rounds, which is claimed to be issued by Sh. Ratnakar Shelake, IRS, Pune which is a 27-point questionnaire on virtual currencies.

Presuming that the notice is legally tenable, in our opinion, any such notice should have been issued, in the first instance, only after the regulatory framework is put in place by the government.

However, irrespective of the legal stance taken by the government about virtual currencies, the Order when issued as a result of such Tax Notice shall indirectly validate the legality of Virtual currencies, wherein the Tax Officer may have to either treat the profits from trading virtual currencies as either business income or capital gains, thereby indirectly providing it legal validity.

Rather irrespective of what legal stance is taken by the Tax Officer subsequently or by the DEA, MoF in the regulatory framework, we analyse each of these 27 points in the questionnaire to assess what the Tax Officer is conjuring to form an opinion regarding virtual currencies in India :

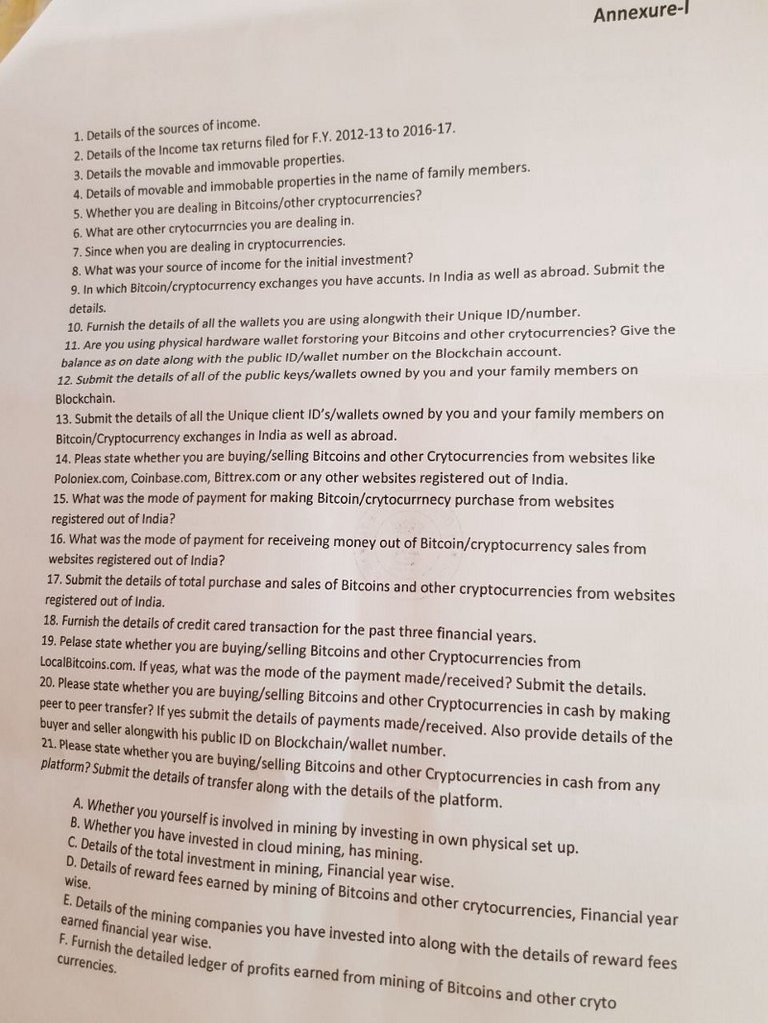

Details of source of Income — This is a general question enquiring about the source of income other than crypto trading income. Primarily this may be to ascertain the source of initial capital investment in cryptocurrencies.

Details of Income Tax Returns filed — This is to ascertain the net worth of the crypto investor, to determine whether he is trading with self earned money or borrowed money.

Comment : Highly recommend to file Income Tax returns, whether mandatory or not with proper disclosures of incomes and gains.

Details of movable and immovable property — This is an add on to ascertaining the net worth the crypto investor.

Details of movable and immovable property in the name of family members — Again, an add on to ascertain net worth of crypto investor and related persons.

Comment : Limit to sharing information only about those family members who are dependent on the crypto traders. Other family members who earn on their own / are self sufficient should not be linked.

Whether you are dealing in bitcoins / other cryptocurrencies — The crypto trader should not deny if he is dealing. However, since the regulatory framework is not in place, “dealing” cannot be defined, it may also include a persons who is not trading but only receiving cryptos as result of his services etc.

What are other cryptocurrencies you are dealing in — The list of all cryptocurrencies “dealt” with should be shared. There should not be any concealment of facts here.

Since when are you dealing in cryptocurrencies — The date of initial investment should be shared. Rather the most appropriate date should be the date on which the transfer from fiat currency account to the crypto exchange account should be mentioned since that is an evidence of confirmed interest by the crypto trader to enter into a proposed transaction of crypto currency.

What was your source of income for initial investment — The source of funds should be clearly depicted. It may be own funds and / or borrowed funds.

Comment : The notion that borrowed funds cant be used in this case, seems incorrect.

In which cryptocurrency exchange do you have account ? In India as well as abroad. Submit details. — A list of crypto currency exchange should be shared.

Comment : The term used in the question is “exchange” however the same have not yet been defined and accepted as “trading exchanges” by any government correspondence. This throws an interesting anomaly that if the Tax Officer defines such trading platforms as exchanges then it provides legal validity that such private website / trading platforms are crypto exchanges, which would then require such trading platforms to adhere to norms applicable to exchanges in India. Pending regulatory framework by government on crypto currency, this anomaly shall remain.

Furnish the details of all the wallets you are using along with their unique ID/ numbers. — Public Wallet details may be shared.

Comment : Currently in the Income tax return there is no field to mention the wallet balance, even as basic as a PayTm wallet balance cannot be separately disclosed. This opens up an opportunity for debate whether such disclosure is mandatory or will the the government revise the Income Tax Return form to offer a separate field for crypto balance and wallet IDs.

Are you using physical hardware wallet for storing your bitcoins and other cryptocurrencies ? Give the balance as of date along with the public ID / wallet number on the blockchain account. — Identical answer to point 10 above.

Submit the details of all the public keys / wallet owned by you and your family on the blockchain — As mentioned in point 4 above, the details should be limited only to family members who are dependent on the crypto trader.

Submit the details of all the Unique client IDs / wallets owned by you and your family members on bitcoins / cryptocurrency exchange in India as well as abroad. — The point to note is that the details are being asked for India as well as abroad. In case the cryptocurrency balances are held in crypto exchanges / platforms which are not registered in India, Foreign Exchange Management Act (FEMA) provisions may be applicable.

Comment : The disclosure under FEMA guideline can be provided however as per these guidelines any payments from or to any country outside India, in fiat currency, are to be categorised under a certain RBI purpose code (an exhaustive list defined by the RBI). However pending the regulatory framework and perhaps subsequent updation of the RBI purpose code list, the exchanges of fiat currency for buying / selling of cryptos may be categorised under one of the existing RBI purpose codes. Since Bitcoins and other crypto currencies may be treated as software codes, in very basic terms, the same may be categorised as Software codes as per these RBI purpose code list.

However a more specific category would be required once the regulatory framework is put in place by the government. Though disclosure of the payments or receipts from foreign crypto exchanges for crypto trades should be made mandatory to avoid illicit money flowing into the money system.

Moreover, the concern from the government’s side should be when trade or exchange in non fiat currency happens which circumvents the banking / RBI route put in place currently by the government. It is expected that the proposed regulatory framework shall put in place additional disclosure for non fiat currency trades resulting in flows in / out of the country.

Please state whether you are buying / selling bitcoins and other cryptocurrencies from website like poloniex.com coinbase.com bittrex.com or any other website registered outside india. — Reply in point 13 already covers this question.

What was the mode of payment for making bitcoin / cryptocurrencies purchases from websites registered outside india. — This question is to ascertain whether payments made outside the country are FEMA compliant or not.

Comment : Generally foreign crypto exchanges allow domestic credit cards to be used for buying cryptos, however a key FEMA compliance is missed in this case. It is for the banks, government as well as the crypto trader to ensure that the compliance requirements as per Liberalised remittance scheme ( if value of trade per year is upto USD 250,000) as well as Rule 37BB and Form 15CA requirements of Income Tax Act be complied with. For higher trades approval route method with the RBI may be requested in addition to Income Tax and Customs compliance, if any.

What was the mode of payment of receiving money out of bitcoin / crypto currencies sales from websites outside india — This is to ascertain whether the gains made were in fiat or non fiat currency.

Comment : In case of gains are in fiat currency ( or converted into fiat currency as at year end), the same would need to be part of total income and be subject to tax. In case of gains, in non fiat currency ,currently there is no field in the Income Tax Act to disclose the same however a notionally converted value of non fiat into fiat currency may be disclosed.

Submit the details of the total purchase and sales of bitcoins and cryptocurrencies from websites registered out of india — This is to ascertain gross profits or gains made.

Furnish the details of credit card transactions for the past three financials years — As pointed out in point 15 above, generally purchases outside India are made through domestic credit cards, wherein the current system doesn’t mandatorily capture the disclosures to be made as per FEMA.

The reason for this query may be to connect the credit transaction with the purchases made and ensure FEMA compliance for the same.

Please state whether you are buying / selling bitcoins and other cryptocurrencies from localbitcoins.com If yes, what was the mode of payment made / received. Submit the details. — The key term here is the “mode” of payment.

Comment : Since it is observed that the stated website also offers cash payment against bitcoins buying, the same may be attempted to be captured by the government especially after the demonetisation era. Again, buying cryptos in cash should not apparently be illegal if the bitcoins itself are provided legal validity however the cash source should be disclosed and explainable.

Please state whether you are buying / selling bitcoins and other cryptocurrencies in cash by making peer to peer transfers ? Is yes, submit the details of payments made / received. Also provided the details of the buyer and seller along with the public ID on blockchain / wallet number. — The core of the question is to ascertain cash purchases of cryptos and ensuring that the source of cash is defined or traced back.

Please state whether you are buying / selling bitcoins and other cryptocurrencies in cash from any platform ? Submit the details of the transfer along with the details of the platform. — The core of the question is to ascertain whether any platform is offering cryptos against cash payment.

A. Whether you yourself are involved in mining by investing in own physical setup. — This is to ascertain how the cryptos were procured either by trade or mining method. Since cryptos by themselves are yet to gain complete legal validation, the legal stance on mining of such cryptos shall also be determined post the regulatory framework implementation.

B. Whether you have invested in cloud mining — Same as Point A above.

C. Details of total investment in mining, financial year wise. — Details should be shared with total investment including machines, electricity cost allocable, employee cost, maintenance etc.

D. Details of reward fees earned by mining of bitcoins and other cryptocurrencies , financial year wise — The disclosure should be made, however what is interesting to note, how to tax officer may categorise the reward fees. Since if reward fees is accepted as legit business gains then it validates the entire process of mining, thereby providing a legal recognition to it.

E. Details of mining companies you have invested into along with the details of reward fees earned financial year wise — This is only an attempt to collect information about related mining companies.

F. Furnish the detailed ledger of profit earned from mining of bitcoins and other crypto currencies — Just like Point D above, it would be interesting to note under which head of income, as per the Income Tax Act would such profits be categorised, if the same are categorised as business profit ( whether speculative or non speculative) then it provides legal validation to the process of mining.

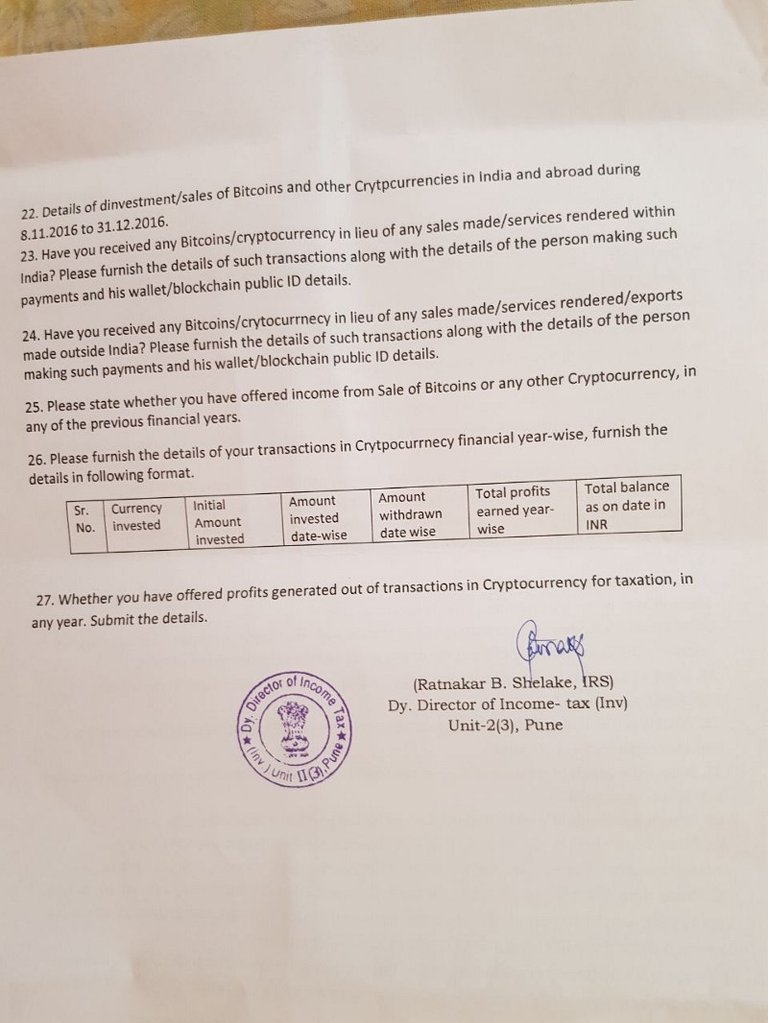

Details of disinvestment / sale of bitcoins and other cryptocurrencies in India and abroad during 8.11.2016 to 31.12.2016. — This is primarily to capture whether the bitcoins were procured from cash. Again, cash buying, though not recommended, isn’t illegal if the bitcoins are defined to be legal subsequently as per the regulatory framework. The issue here is that the cash should be explainable and the source be defined.

Have you received any bitcoin / cryptocurrency in lieu of any sales made / services rendered within India . Please share the details of such transaction along with the details of the person making such payments and his wallet / blockchain public ID details — The government has taken as stance that crypts are not legal tenders in India, hence accepting bitcoins or other cryptos as a result of service or sales are not legit.

Comment : However the same transaction be looked into as a barter transaction. As a precedent, Company Act may be referred to here, wherein shares can be issued against a service and no monetary exchange is needed to legitimise the transaction. A similar case may be considered for payment in cryptos against sale or services, however subject to proper discharge of GST liability.

Have you received any bitcoin / cryptocurrency in lieu of any sales made / services rendered/ exports made outside India ? Please share the details of such transaction along with the details of the person making such payments and his wallet / blockchain public ID details — In addition to the point 23 above, the point to observe here is “outside india” which signifies that in addition to the compliance as per Income Tax and Indirect Tax law, FEMA guidelines may also be complied with, as detailed in point 13 above.

Please state whether you have offered the income from sale of bitcoins or any other cryptocurrency in any of the previous financial years. — This is rather intriguing! If the income from cryptos is added to the total income of the crypto trader ( assessed as per income tax act) then it legitimises the overall transaction of crypto trading, however it is not added then it results in bigger non compliance.

Comment : The issue is bigger from the government’s viewpoint, if the income is allowed to be added to the total income of the assessee and be part of the income tax return, then whether it is taxed as capital gains or as business profits shall result in legitimising the entire world of cryptos. However if the same is not added then the gains or profits and the taxation thereupon shall result in loss of government revenue. Only in case the government outrightly bans all cryptos trade ab initio can the crypto traders be treated as money launderers and be tried under Prevention of Money Laundering Act, however had that been the case the government would not have issued precautionary notifications, rather would have issued an outright ban in the first instance itself, which has not been the case.

Please furnish the details of your transactions in cryptocurrency financial year wise, furnish in the following format

This should be disclosed.

Whether you have offered profits generated out of transactions in cryptocurrency for taxation, in any year. Submit the details — Please refer to point 25 for complete details.

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://medium.com/@blockchainlawyer.india/what-the-indian-tax-officer-wants-to-know-about-your-bitcoin-gains-6a9302054dfd

Congratulations @blockchainlaw91! You received a personal award!

You can view your badges on your Steem Board and compare to others on the Steem Ranking

Vote for @Steemitboard as a witness to get one more award and increased upvotes!