by Josh Olszewicz, 07 Jul 2018

The total market cap for all cryptocurrencies and assets currently stands at ~US$250 billion, unchanged since the beginning of the quarter. The total market cap peaked at the start of this year, at around US$800 billion, followed by a 3 month decline. The total market cap then rebounded from April to May, before giving up those gains just as quickly.

Source: https://cryptolization.com/

Source: https://cryptolization.com/

Despite the tumultuous volatility throughout the quarter, many coins closed the second quarter with a higher price than the beginning of the quarter. Positive movers for the period include Decred, ZRX, EOS, Augur (Rep), ByteCoin, BinanceCoin (BNB), Aeternity (AE), and Tron (TRX).

EOS, VeChain, Ontology, Tron, and Aeternity all released independent new blockchains this quarter after migrating from an ERC20 token. NEO, dubbed the Chinese “Ethereum-killer”, suffered some of the biggest losses this quarter, almost halving its market cap. The ICO boom fueled much of Ethereum’s bullish price action. Time will tell if ICOs listed on NEO will also increase demand for the asset.

Source: https://coin360.io/

Source: https://coin360.io/

Bitcoin’s relative market dominance has steadily risen throughout the quarter but remains much smaller than before ICO mania ensued. As ICOs or coins are continually added to the ecosphere, Bitcoin is unlikely to ever return to >80% market cap dominance. If Bitcoin is able to upgrade and improve features, like private and confidential transactions, assets with a weaker value proposition will likely diminish in value.

Source: https://coincodex.com/market-overview/

Source: https://coincodex.com/market-overview/

Ethereum’s relative market dominance has increased throughout the year. This rising trend should continue unabated as the Ethereum protocol gains importance, with second layer protocols emerging from ICOs and ERC tokens. Most of the largest ICOs by money raised continue to occur on the Ethereum blockchain.

Source: https://coincodex.com/market-overview/

Source: https://coincodex.com/market-overview/

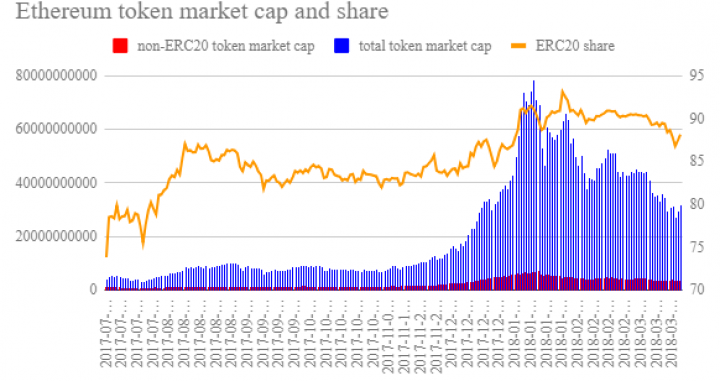

The market cap for all Ethereum based tokens is ~US$30 billion. ERC20 tokens hold ~90% of that total market share, which peaked at 93.15% on January 26th, 2018. Tether, a non-ERC20 token, has had an increasing market cap over the past year, now standing at US$2.75 billion.

Source: https://medium.com/@amincad/market-share-of-ethereum-based-tokens-grows-to-91-fdefadfd9f6e

Source: https://medium.com/@amincad/market-share-of-ethereum-based-tokens-grows-to-91-fdefadfd9f6e

Lack of Consensus Rally

On May 14-16, one of the biggest conferences of the year, Consensus, was held at the Hilton in Midtown New York City. Despite the record attendance of ~8500, many there (including myself) felt the conference offered a lackluster experience, especially considering the US$3,000 per person ticket price. The true value of many crypto conferences lies in the ease of networking and meeting others in the industry, which seemed lacking this year. However, there were some highlights.

On a panel, Jesse Powell, the CEO of Kraken, and Erik Voorhees, the CEO of Shapeshift, discussed how they were forced to leave New York state due to the regulatory overreach of the Bitlicense, created by Benjamin Lawsky. Xapo and Square, both companies involved with wallet services, received their Bitlicenses in June.

Powell said that San Francisco-based Kraken would have been forced to “disclose all the information about our entire global client base to the state of New York” which is "potentially illegal" under the privacy laws of other countries, especially with the release of EU’s General Data Protection Regulation (GPDR).

Voorhees also commented on the hurdles of the Bitlicense, remarking “here we are two miles from the Statue of Liberty and you cannot sell CryptoKitties in the state without that license. That’s the absurdity of what’s happened here.” He added that crypto exchanges and services have had to play "regulatory hopscotch" to be able to operate their businesses.

Consensus was also predicted to be loaded with announcements from institutional investors entering the crypto market. The most impactful announcements for the institutional roadmap were a slew of custody solutions. Japan-based Nomura announced a joint venture in partnership with Ledger and Global Advisors to increase institutional investment. Earlier in May, the New York Stock Exchange (NYSE) also announced that a Bitcoin trading platform was in the works.

The exchange Gemini, which operates with a Bitlicense, announced the addition of ZEC to the platform. ZEC is one of the first coins with a privacy feature to be added on a fully licensed U.S. exchange. Other privacy coins like XMR and DASH remain unlisted on a licensed U.S. exchange. In June, the U.S. Secret Service recommended regulation of all privacy coins, including ZEC, XMR, and DASH.

Japan's Financial Services Agency has already pressured exchanges to drop ZEC, XMR, and DASH, citing criminal activity. Coincheck, the most popular Japanese exchange, delisted all three coins in May.

EOS joins the Ethos

EOS completed the longest running ICO and highest raise of any ICO this quarter. After raising ~US$4.2 billion, with an average token price of US$5.74 for all public rounds, the platform went live on June 14th. The EOS market cap now stands at US$7.3 billion.

However, the EOS saga has been rocky since the beginning. Dan Larimer, EOS CTO, hastily announced a bug bounty program on May 28th after being asked to in the EOS telegram chat. Many users were concerned this had not been announced much earlier, during the year-long ICO. There was also concern that the US$10,000 reward per bug found was too low considering the network’s value. One programmer found 12 critical bugs, which were patched before the platform's release. Only hours after being live, a bug halted the platform for five hours.

The network took several days for 15% percent of all tokens to stake a vote for a Block Producer Candidate (BP), with several users refusing to vote, citing security risk by unnecessarily exposing private keys. Greymass, a software voter, has been released, but many users prefer the security of a hardware wallet to generate private keys.

EOS also came to fruition with a constitution, written by “blockchain governance expert” Thomas Cox, which was to be followed by each user and block producer. Of the 19 articles listed, “Article XVII - Termination of Agreement” is among the most alarming to EOS holders because it allows wallets to be auctioned to other users after three years of inactivity.

Several articles also refer to “arbitration,” with one such action occurring only days after launch on June 22nd. With an "Emergency Measure of Protection Order", EOS directed it’s BPs to censor transactions from 27 accounts with no due process or reason given. One BP, who did not comply with the arbiters wishes, was harassed and threatened with a lawsuit.

Larimer has since announced that Block.One, the designer of the EOS project, has decided to scrap the current constitution and start anew. In the EOSIO Gov telegram group, Larimer commented, “forcing people into an unknown arbitration system for undefined reasons is a fast way to cause people to run.”

Last week, Block.One decided to use it’s EOS share to vote for the BPs directly. Jackson Palmer, the creator of DogeCoin, gave some harsh commentary, “So Block.One, who claimed to have no involvement in the launch of the EOS mainnet, are now going to use the 10% of the token supply they own to influence the list of block producers. Interesting.” EOS users also raised concerns that Block.One’s involvement in BP voting will increase centralization for the network.

Despite a bumpy start, several opt-in airdrops have been released or announced since the mainnet went live. One airdrop, EON, was difficult to obtain according to several users. Similar to ETHfinex for ERC20 tokens, EOSfinex will likely list many or all of these airdrop tokens for trading. Overall, Transactions on the network remain almost non-existent.

Not A Security

On June 15th, William Hinman, the Director of Corporation Finance at the U.S. SEC, gave a speech at the Yahoo Finance All Markets Summit in San Francisco. The discussion was specifically focused on determining whether or not crypto assets are securities. Hinman specifically commented on Bitcoin and ETH as not representing securities, citing the decentralized nature of both networks.

“And putting aside the fundraising that accompanied the creation of Ether, based on my understanding of the present state of Ether, the Ethereum network and its decentralized structure, current offers and sales of Ether are not securities transactions.”

Current SEC chair Jay Clayton has already said, “I believe that every ICO I have seen is a security,” and has implied that ETH is not a security, although ETH did have a token sale of its own in 2014.

Hinman went on to say that enterprises, or ICOs, created and developed by a third party with an “expectation of a return” for the investor are more likely to represent securities. Regardless of whether an ICO represents a utility token, most ICOs fall under the umbrella of centralized enterprises where profit comes from the efforts of a promoter or third party, as stated in the Howey Test.

In May, ex-CFTC chairman Gary Gensler said that he believed there was a “strong case” that ETH is a noncompliant security. The comment was responded to by Andreessen Horowitz and Union Square Ventures, among others, who asked the SEC for safe harbor from securities law, suggesting that the law does not apply to ETH due to its decentralized nature. Joseph Lubin, co-founder of Ethereum, has long said he’s “extremely comfortable” that ETH is not a security.

The regulatory clarity was also seen as positive news by CBOE president Chris Concannon who told Bloomberg, “this announcement clears a key stumbling block for Ether futures.”

Even though the news was perceived as positive, lawyers across the cryptosphere, including Drew Hinkes and Stephen Palley, were quick to remind the community that a speech is not law but a good indication of the SEC’s regulatory position. The next hurdle is properly defining what “sufficiently decentralized” truly means. Palley added that “a bunch of ICOs will get taken down” for not complying with securities law.

Marco Santori, the creator of SAFT (simple agreement for future tokens), said the news was, “exceptionally bad news for custodial providers, exchanges and OTC desks who trade tokens” because they “will need to register as National Securities Exchanges or alternative trading systems and stop accepting non-accredited users.”

Overall, the regulatory discussion surrounding ICOs should not be a surprise. Most ICOs have now opted to incorporate in Switzerland or Singapore, have begun to use KYC/AML procedures, and do not accept non-accredited U.S. investors. More and more ICOs are now moving to private sales exclusively without a public sale. The Telegram ICO, the largest individual ICO to date, raised US$1.7 billion privately and was never sold to the public.

Whether or not the SEC will seek action against the Ethereum Foundation remains an open question. Preston Byrne agreed with Gensler that ETH was a security and that “decentralization does not terminate the initial investment contract”. He adds that “decentralization is legally meaningless,” at least currently.

As Santori mentioned, exchanges and custodians are now at high risk of being in violation of securities laws. No exchanges currently in operation are registered as National Securities Exchanges. From an enforcement perspective, it is more effective to bring action against exchanges creating the secondary market instead of ICOs one-by-one.

The Boogeyman Cometh?

Tether was designed as a stable coin with a 1:1 peg to US$1.00. Funds held on the tether blockchain represent an equivalent in a Tether bank account. The main concern for many skeptics is a lack of audit on the bank funds held by Tether.

Tether’s current market cap accounts for 1% of the total crypto market cap. As the cryptocurrency market has fallen broadly, a safe-haven, like the Tether stable coin, has gained increasing importance for investors wishing to shield themselves from market volatility.

The Bearish Boogaloo 8On June 15th, Tether released a transparency report produced by Freeh, Sporkin & Sullivan (FSS) LLP. While not an audit, the report concluded that, “FSS is confident that Tether’s unencumbered assets exceed the balance of fully-backed USD Tethers in circulation as of June 1st, 2018.”

A non-peer-reviewed academic paper was also released earlier in the month claiming that “Tether is used to provide price support and manipulate cryptocurrency prices” citing an increase in Tether issuance during troughs in Bitcoin price. The paper also noted, “the buying of Bitcoin with Tether also occurs more aggressively right below salient round-number price thresholds where the price support might be most effective.” This is a well-known phenomenon known as psychological support or integer bias and occurs regularly in all markets, without the use of Tether.

Last week, Bloomberg released an article entitled “Crypto Coin Tether Defies Logic on Kraken’s Market, Raising Red Flags”. The article cited suspected problems including specific order sizes to five decimal places, large Tether orders failing to move prices, and wash trading.

Kraken immediately responded in a blog post entitled “On Tether: Journalists Defy Logic, Raising Red Flags” where they deny any manipulation claims adding that their “daily USDT volume is less than 0.1% of aggregate daily volume across all competitors.” Kraken also mentions that “large trades may result in no change or similar changes in price because there is a much larger buy or sell order in the order book that has not been filled.”

To Q3 (And Beyond)

In general, news throughout the cryptosphere slowed in Q2 with subdued prices broadly. Key upcoming announcements for the remainder of the year include the possibility of a Bitcoin ETF as well as a CME or CBOE Ethereum futures contract. Other exchange related news includes which coins will be added to the exclusive ‘listed on Coinbase’ club, and whether or not Coinbase will create an ERC20 token trading platform similar to other exchanges in the space.

Technicals for most coins show a sustained bear market with the suggestion of a pending relief rally. Almost all coins are being tightly held in a downward channel. As always, watching the movements of the top currencies like Bitcoin and Ethereum will be the most valuable as they will likely dictate the entire market as a whole.

my dear friend, let's see how the site behaves, very useful as always your information ... As always setting trends ...

thanks for the imformation

It's been mentioned a lot in the sub lately but you should also take a look at Oyster (PRL), main net and airdrop coming in April