what is blockchain technology?” and you get 10 different answers — even in the crypto-scene itself. The best approach to forming a true understanding blockchain is by understanding the underlying technologies step-by-step.

in this post, I will go over the three main components of blockchain technology: the blockchain itself, peer-to-peer networks and consensus mechanisms. Bitcoin would not be able to exist if any one of these components did not exist. Let’s start with the blockchain.

Understanding the blockchain itself:

In short, a blockchain is just a way to structure data. That’s all there is to it. It is a ledger: A file that keeps track of accounting records.

This file is comparable to a book that is never finished.

Each page in a book has information written on it and a page number on the bottom. Because of this page number, you immediately know where the page belongs in the book. Page 49 is obviously found between page 48 and 50.

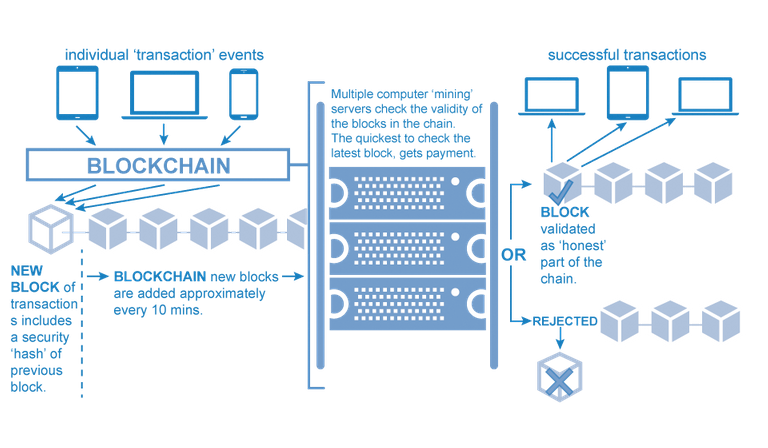

Just like pages, blocks are filled with information. Although blocks don’t have exact numberings, they have a timestamp, which fulfills the exact same function. A new block is always added after the block with the most recent timestamp. As such, a chain forms

In Bitcoin’s blockchain, the blocks contain information about transactions in Bitcoin. The block states who sents which Bitcoins to whom.

As the blockchain has been used to keep track of the movement of all Bitcoins since their inception, the ledger can be checked to know exactly who owns which Bitcoin at any time. The ‘who owns what’ at any time, is what we call the current ‘state’ of the blockchain.

A transaction only occurs once it is included in a block and added to the chain. Hence, when a block is added to the chain, the state of the blockchain is updated. After all, Bitcoins have moved.

This means that if I want to validate whether someone actually made a transaction to me or not, I have to be able to check the state of the blockchain. To be able to do this, the ledger has to be publicly available. This is where peer-to-peer networks come in.Understanding the role of peer-to-peer networks

Peer-to-peer (P2P) computing or networking is a distributed application architecture that partitions tasks or workloads between peers. Peers are equally privileged, equipotent participants in the application. They are said to form a peer-to-peer network of nodes.

Peers make a portion of their resources, such as processing power, disk storage or network bandwidth, directly available to other network participants, without the need for central coordination by servers or stable hosts. Peers are both suppliers and consumers of resources, in contrast to the traditional client-server model in which the consumption and supply of resources are divided. Emerging collaborative P2P systems are going beyond the era of peers doing similar things while sharing resources, and are looking for diverse peers that can bring in unique resources and capabilities to a virtual community thereby empowering it to engage in greater tasks beyond those that can be accomplished by individual peers, yet that are beneficial to all the peers.

- Understanding the consensus mechanism

A peer-to-peer mechanism was used in ’99 already by Napster.

The blockchain, too, already existed before Bitcoin.

The ingenious part of Satoshi Nakamoto’s, the mysterious, anonymous founder of Bitcoin, white paper was combining the two with a consensus mechanism based on cryptography. The consensus mechanisms is where the real magic happens: it allows nodes in a peer-to-peer network to work together without having to know or trust each other.

Now, if you didn’t quite catch that, the consensus mechanism is simply a set of rules, which is agreed upon by the nodes in the network by running the software of the network. These rules make sure the network works as intended and stays in sync.

The consensus protocol sets rules on:

How blocks are to be added to the chain,

when blocks are considered to be valid, and

how conflicts of truth are resolved.

Adding blocks to the chain

Different blockchains add blocks to their chains in different ways. The most-known consensus mechanism is Bitcoin’s Proof of Work (PoW).

The first rule of Proof of work is that one block should be added to the blockchain, on average, every ten minutes.

The process to facilitate this is called ‘mining’. Nodes that try to add a block to the chain (called ‘miners’) use computational power of their computers to try and solve a cryptographic ‘puzzle’. The rules state that only when this puzzle is solved, a block can be added to the chain.

The miner that solves the puzzle, and therefore ‘mines’ the new block to add to the chain, is rewarded by the network. A predefined amount of new coins is created and given to him, together with the transaction costs of all transactions contained in the block.!

( )

)

Bitcoin’s Proof of Work is not the only consensus mechanism. Proof of Stake (PoS) is also commonly used in distributed ledgers. In a Proof of Stake based mechanism, one can ‘stake’ his coins for a chance to be picked to add the next block. In a sense, a staker says: “ I bet my coins that I add this block correctly”. If he lies, he loses his coins.

There is a larger debate on which consensus mechanisms is best. Still, regardless of how the block is created, other nodes in the network still have to be able to decide on whether the block is valid or not.

Conclusion

The above should be seen as a very brief introduction to how distributed ledgers work. You might now understand why “blockchain” is a bit of a misnomer for the distributed ledgers we see today.

However, next time someone mentions blockchains at a party, please don’t do what I just did and go: “Hey man, a blockchain is only a way to structure data. I think you mean to refer to a distributed ledger used for record-keeping, which is hosted on a peer-to-peer network of participating nodes and miners whose cooperation is both enabled and governed by a consensus protocol which states rules of the network.”

Instead, it might be time to accept that the term has evolved to become an overarching concept to indicate the synthesis of the technologies that make distributed ledgers possible.

Good explanation. Its interesting that the success of Bitcoin has made blockchain technology popular but yet the Bitcoin whitepaper does not mention the term blockchain at all.

what ever it, any technology came from success after get popularity