Last night I attended a meetup in San Francisco with a theme of "Blockchain For Social Impact & Financial Inclusion". It was organized by the Stellar SF meetup group and hosted by Digital Garage who graciously provided pizza and beer for 200+ attendees - thanks guys! It was almost like clamoring to get into a popular ICO with a long line out on the sidewalk from half an hour before. A lot of people walking by were asking what the heck was going on. I was pleasantly surprised that most seemed to know what blockchain or cryptocurrency was. As over 500 people RSVPed for the meeting so I'm pretty sure some were left out in the cold because there wasn't a venue big enough for that many people (even if traditionally a 50% turn out is good for a meetup).

It is really impressive so many people are interested in just a meeting and of the few people I did speak to it seemed like they were all interested in how we can use the blockchain to those ends - social impact and financial inclusion vs just HODLing and getting rich.

The meeting was divided into two parts, one a talk about SureRemit and the rest a panel discussion followed by Q&A on the main theme.

SureRemit

This talk was given by Samuel-Biyi an entrepreneur from Nigeria who helped create Jumia the Nigerian equivalent of Amazon.com, and then built SureGifts a gift card platform that delivered funds as email, SMS, or physical gift cards redeemable at specific merchants or businesses. For example, a gift card could be tied to medical services, or for a specific only merchant like Amazon (or the local equivalent). The service proved very popular and ended up as a way to pay remittances across borders. So they decided to do the same but based on the blockchain.

Samuel noted that as vouchers they were able to provide the service to purchasers completely at face value with no surcharges. That is because the vendors would subsidize costs as SureGifts was driving business to them - something they would normally pay quite a bit for. That's why in the US those coin counting machines that customers can use for their buckets of coins are completely free, but only if you get paid in vouchers for retail stores. If you want actual cash back they take a fairly hefty percentage of the money counted.

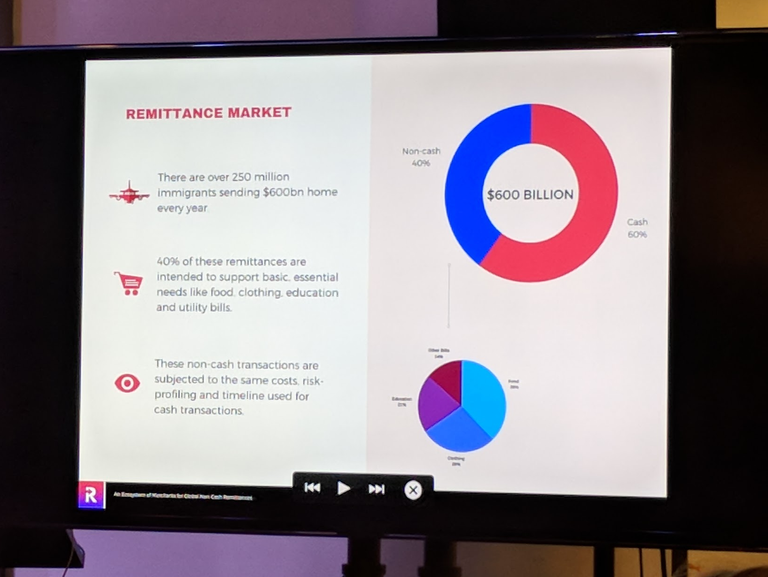

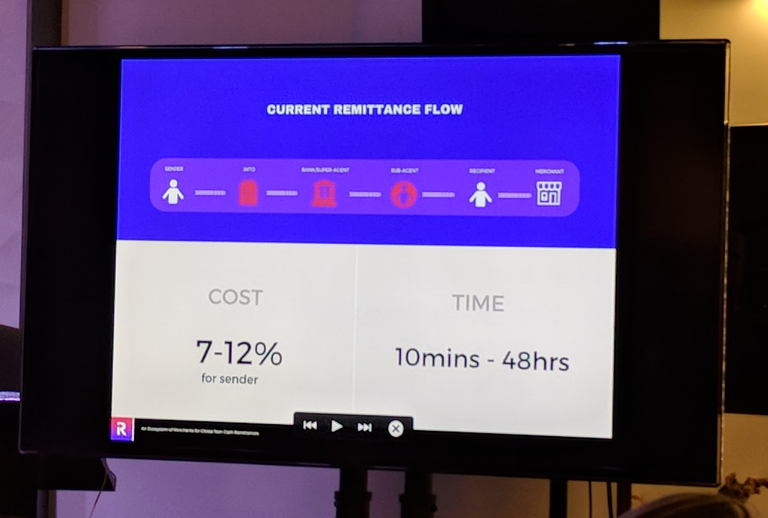

In tackling the remittance business they hope to drive costs to zero and make them very fast. Compare that to the 7-12% fees charged by traditional businesses, and the 10 minutes to 48 hours processing time they take. With blockchain they could be down to seconds and have complete transparency. But for now they are compeltely sticking to non-cash use - their RMT token will be used to exchange at a market rate for an equivalent fiat amount of goods or services.

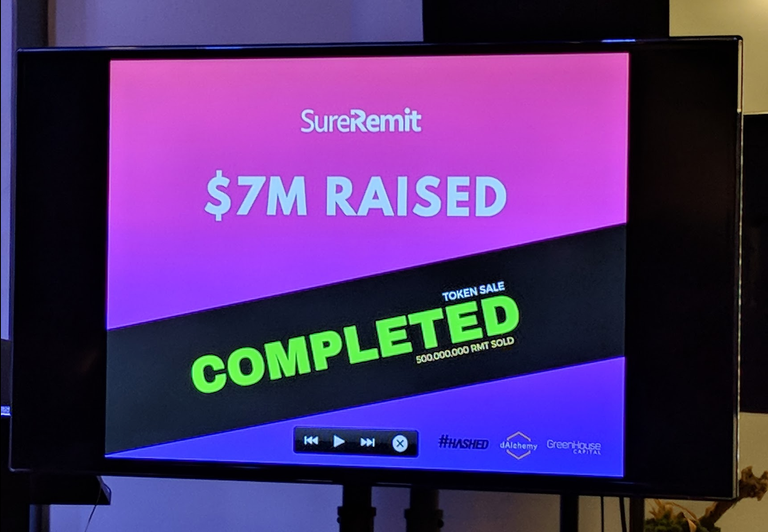

SureRemit is supported by Alchemy, Hashed, and Greenhouse Capital. Their ICO was 500M tokens and they raised $7M in just two days. They hope to have a live version rolled out in March, and go global to the Middle East and India in Q3, then Latin America in Q4. Their number on task is to add players to take fiat in exchange for RMT, and to add merchants to accept the RMT in exchange for gift cards.

A recurring theme of the evening was the difficulty of getting consumer to pay cash for Crypto, and then vice versa, also know as the on-ramp/off-ramp problem. But making the off-ramp be only about receiving goods and services they do simply it for the end customers. They could and should have zero knowledge that stuff is happening on the blockchain beneath them.

Panel session

The panel session consisted of

- Boris Reznikov - Stellar, Partnerships - Moderator

- Adeoye Ojo - co-founder of SureRemit

- Connie Gallippi - CEO and Founder of BitGive foundation

- Ben El-Baz - Stanford University

- Zubair Ahmed - CTO of Give Foundation

Among areas that the panelists named as important in achieving the goal of social impact and economic inclusion they listed:

- land registry

- remittances

- voting

- supply chain tracking

- incentivized carbon removal

- elimination of corruption through transparency

- achieving multi-generation impact beyond a single lifetime

- securing identities

Zubair commented that "Proof of Work is not going to work" and that we need to build apps that get people using tokens, not HODLing. Adeoye added that although there could be some speculative aspect to the value of their RMT token, actual usage would provide a floor and that floor would increase as popularity and use increased .

Connie emphasized that they need to create apps that everyday users can utilize. The prime issue for her was onboarding/off-boarding/last-mile conversions of crypto to and from fiat, or actual goods and services. She mentioned that Square's announcement of their "cash out" allowing ree Bitcoin payments (presumably mostly off-chain) is a huge step in the right direction and others would be sure to follow soon.

Ben talked about how not everything in a blockchain app has to be on the blockchain. On the blockchain functionality allows user control of data, de-siloing data, avoiding double-spend. However many things can be done off-blockchain with many benefits.

Boris (from Stellar) pitched in that Stellar allows you to "digitize fiat currency" backed by real entities. In later 1:1 discussion with me he admitted this does not work for USD yet, only Euros and some other international currencies. He also pointed that the "anchors" that back those digitized funds are far more reputable than opaque entities like Tether which some people believe is either on the verge of collapse or at best a complete scam that needs to be investigated. However, you are still subject to the possibility of a bank going bust and hoping that there is insurance somewhere that could cover your unsecured losses. He also pointed out that a digitized fiat asset from one anchor on Stellar is not equivalent to an identical amount of fiat from another anchor. There is no guaranteed exchange between them it's like a Bank A:EUR IOU vs Bank B:EUR IOU and you'd have to get them to agree to exchange.

In the audience questions, someone asked what is a path that normal people can use to get others involved? Panel answers included:

- more people describing the technology in a way that is not techie

- more great speakers like Andreas Antonopoulos

- it's an innovators dilemma - where something exciting an new is there which could put all those who ignore it out of business, but adopting it could destroy your own business. Ben mentioned a pre-sale book on Amazon called After Google that describes a post-Google world where the blockchain takes over

- Zubair said many people simply don't need to know about blockchain, just have great products that work well using it underneath (like you don't need to know HTTP and BigData to use Amazon.com). But they probably do need to know about cryptocurrency and new economies - that there are such things.

- cryptocurrencies can represent the separation of concerns

Another question addressed the issue of speculation ruining the economies and adoption of new blockchain projects. Should teams try to adopt methods that discourage speculation and HODLing-like behavior?

The panel generaly thought it would be nice if you could, but didn't know how to do that or that anyone had managed to do it so far. As an aside my idea on this is that you could have a token with economics such that unused tokens "rot" in some way. For instance when spending tokens a transaction fee could be levied based on the average amount of time funds in the source address had been there. A reasonable threshold would not penalize short term deposits but beyond that the spendability of the coin would decrease quite rapidly. This would encourage velocity of funds in the system. For sure their are flaws - you'd need a system where people couldn't just move funds around between their own wallets to avoid fees. But I think there is probably some other system that could achieve a similar "token rot" effect without an easy workaround to defeat it.

When asked what the panelists expected to see in ten years if all the current projects were successful they mentioned:

- A global real-time dashboard showing what is happening with relief and charity around the world.

- Users with true ownership of own data

- Cost of remittance goes to zero

- Borderless currencies (Ben noted that people in Venezuela he knows are actually being paid in Bitcoin)

An audience member asked where last mile on/off-ramp problems being discussed? The only suggestion was from the moderator to look at the Stellar public channels on Slack

The final question was a weighty one

How do we actually get areas that are corrupt to use blockchain, do we need a people's revolution?

I didn't hear any great answers but my thoughts are:

- the people's revolution is for people to actually start using blockchain technology as a defacto solution regardless of what "the authorities" or trumped up dictators say.

- ultimately the only barrier to such a thing should be the law and in most places, if enough people ignore a law then it becomes either unenforceable or ends up being eliminated.

That's a similar thing to what happened in the US with the prohibition. Thanks to jury nullification prosecutions against bootleggers became extremely hard to enforce, juries simply refused to convict which is their right no matter what the evidence.

If people power and equivalents of jury nullification in places with rule of law does not work then perhaps international law, treaties, and trade agreements (which often have more clout between countries) could be used to require countries to allow blockchains and accept the legality of blockchain based records - like land titles and "bank" balances. However, that assumes the establishment and old world order is ready to be so bold and almost certainly seal its own fate in the process.

I can't believe I missed this event. Sounds like it was nice.

I am really excited about this space. We encourage you to check out our work at the Digital Reserve. We are really embarking on a journey that may interest you. Let us know what you think. Our focus is really to combat predatory lending and high interest rates through a borrower focused system.