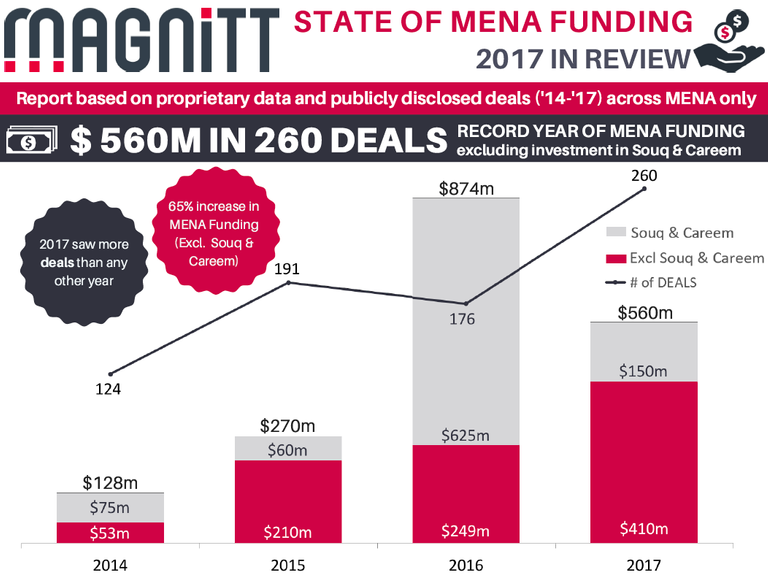

MAGNiTT, a platform that tracks and reports developments in the MENA entrepreneurship space, starts 2018 by taking a look at the year gone by and how it treated the region’s startups. Releasing its annual State of MENA Funding report, MAGNiTT finds that in 2017, MENA’s startups attracted US$560 million of investment across 260 deals. This investment activity constitutes a 65% rise from 2016 (excluding amounts raised by Careem and Souq.com), making 2017 “a record year” for the MENA entrepreneurship world, according to MAGNiTT. MAGNiTT’s State of MENA Funding reports are based off proprietary data and publicly disclosed deals covering the period 2014-2017 across MENA.

“All in all, 2017 had many positives. A record year for deal flow; a record year of funding when stripping out investment in Souq and Careem; increased awareness across the region, and new entrants into the ecosystem,” says Philip Bahoshy, founder and CEO, MAGNiTT. Commenting on signs of growth and maturity of the overall ecosystem, he notes that in terms of number and breakdown of deals, 2017 saw 179 early-stage investments, up 75% from 2016. “In addition, as the ecosystem matures, we have seen more Series A and later stage investment deals than any previous year with Series A investments accounting for close to $100 million,” he adds. Among other noteworthy firsts in the report is the emergence of a record Q2, Q3 and Q4 period for MENA business world in terms of investment amounts and number of transactions. Further, 2017 also saw most number of deals undertaken than any previous year of study, across MENA. The top five investments recorded were $150 million in Careem, $90 million in Starz Play Arabia, $41 million in Fetchr, $20 million in PayTabs, and $12 million in Wego. With respect to sectoral performance, e-commerce and fintech continued to retain top positions in 2017, accounting for almost 12% of all deals each. The regional Food & Beverage companies saw the largest increase (3%) in deal flow, while technology enterprises (startups driven by proprietary technology, but not in nature of e-commerce and fintech) reported a dip of 2.5% in deals.

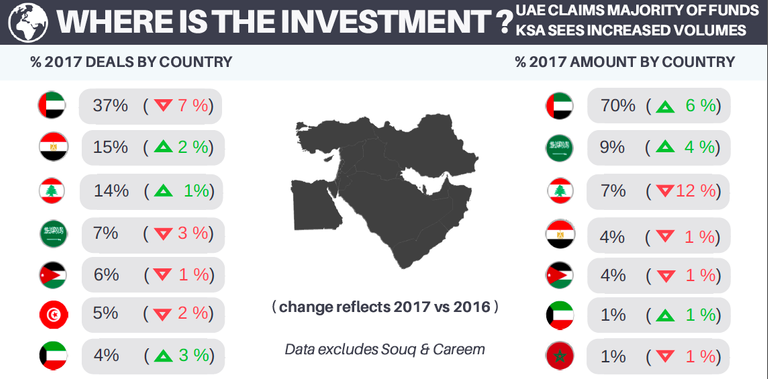

As for key geographic trends, UAE startups continue to dominate the region with 70% of all investment amounts. Saudi Arabia recorded largest increase in investments (up 4% from 2016), and Lebanese startups saw biggest drop in investments- down 12% from 2016. As already highlighted in the individual quarterly reports of 2017, 500 Startups has emerged as the most active VC firm in 2017- deploying investments in over 30 startups following the launch of their MENA Falcon Fund last year. Middle East Venture Partners followed close behind with 14 deals, and KSA-based VC’s such as Raed Ventures, Riyad TAQNIA Fund, and others, also made their presence felt in 2017 as active investors.

Talking about what MENA startups can expect in 2018, Bahoshy says, “Much of the conversation in 2017 was focused on fundraising, not only for startups but for VCs, as well. I expect the current trend to continue into 2018. There continues to be strong deal flow across the region, and many of the existing VCs are likely to deploy further capital into portfolio companies as well as new investments as they close out their new funds.” He is also optimistic about governmental support for the region’s startups, and anticipates that “governments will continue to fuel entrepreneurship through new legislation and initiatives, as we continue to see new accelerator partners enter the region including Techstars, Krypto Labs and 500 Startups' MENA Dojo.” To access the full list of startups funded in 2017, and a detailed presentation on 2017 investment trends part of this report, visit MAGNiTT’s official page here, and subscribe.

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://www.entrepreneur.com/article/307485