The following passage is an excerpt from a chapter of my upcoming e-book, "Conscious Consumption"

When in conversation with friends or in passing I've often heard the catch-phrase, "think of it as an investment". But based on these conversations and interactions, and the "assets" often referred to, I'm convinced that many individuals do not know what actually constitutes an investment.

As defined by Oxford dictionary, an investment is "a thing that is worth buying because it may be profitable or useful in the future."

However, I don't believe this definition to be quite clear, or even fully accurate. The financial education and news outlet, Investopedia, expands on Oxford's definition by adding that an investment is:

"an asset or item (time, money, effort, etc.) acquired with the goal of generating income or appreciation.

In an economic sense, an investment is the purchase of goods that are not consumed today, but are used in the future to create wealth. In finance, an investment is a monetary asset purchased with the idea that the asset will provide income in the future or will later be sold at a higher price for a profit."

I view this last clause, the likelihood of the asset to increase in value, as paramount to the definition of an investment.

An investment always concerns the outlay of some asset today (time, money, effort, etc.) in hopes of a greater payoff in the future than what was originally put in.

In my mind, an investment is a liquid or material asset with cash value, that doesn't typically (but not always) have an upkeep cost, and is likely to appreciate, rather than diminish in value. Anything that costs you money is a purchase or an expense, or both. Automobiles are an example of the later, as they decrease significantly in value as soon as you drive them off the lot, and have a lot of recurring fees (insurance, gas, oil changes and other maintenance, etc).

The same can be said for houses, which are more commonly viewed as an "investment" by the public. There are certainly many costs associated with their upkeep, and the majority of homeowners do not make a profit when selling their house after years of owning it. The value typically rises a little bit higher than inflation, so one can view a house as a hedge against inflation. But seller fees and volatility in the housing market are variables that will impact profitability, and there is no guarantee of a profit when you are ready to sell.

Home-ownership can provide utility in the psychological and emotional sense by providing greater comfort and peace of mind. It can also wise, practical, and pleasurable to own a home, rather than rent. But, on the other hand, it could also cause you stress, worry and tons of time, money and energy. In other words, homes could be viewed as a liability, depending on the particular individual and respective situation.

This is where I take issue with possessing too many material goods. Ownership of homes, automobiles or too many other physical possessions often crowds one’s mental and physical space, and takes up time and energy, often preventing the individual from utilizing any of these items to the extent they had originally envisioned when purchasing. The takeaway is that the less material goods one purchases, the more money they have freed up to allot towards actual investments that don’t cost time, energy and money to maintain. The ideal strategy is saving first, with the benefit of being able to afford what you need later on. By not buying on emotion, you may be able to find the item or service for a better value later, or realize it's a non-essential altogether.

Banks

Obviously, the first place one typically thinks of to store their hard-earned money is with a financial institution such as a bank or credit union, as they provide the most liquidity (the degree to which assets can be quickly bought or sold in the market) for the consumer. However, the conscious consumer should not consider this a viable option for housing the majority of their "worth", just based on principle alone.

Most of the nation's largest banks have a long-standing history of corruption, or at least a history of engagement in practices that violate the conscious consumer's moral code of conduct. Just as one example, most recently Wells Fargo was caught up in a fraud scandal in which it opened millions of unauthorized savings and checking accounts on behalf of existing clients without their consent.

And though no individual convictions were ever completed after the 2008 housing collapse ( we have state and federal government's susceptibility to bribes to thank for that), it's basically public knowledge that the higher-ups in America's largest banks repeatedly brushed off or fired lower-levels employees more privy to what was going on when those individuals attempted to warn them.

Regional credit unions are a better option for storing some money, as they are less corporate-centric, and usually offer at least some small incentive or reward for keeping an account active, or frequently using a checking card, such as cash-back bonuses or waived ATM withdrawal fees. Taking these benefits into consideration, credit unions should be seen as the better option, or at least the lesser of two evils.

However, it is not recommended that accounts with credit unions be used as the primary location for the storage of wealth. Out of necessity for how society operates, it is only practical to keep some funds in a bank account, as it will provide the individual the most liquidity for everyday transactions like withdrawals or instant deposits. But just like larger, national and international banking firms, only a small fraction of your money, and the total amount of what they have on the books, is actually reserved in the physical, brick-and-mortar location. The Federal Reserve upped this amount in 2019, pushing the limit for banks with more than $124.2 million in deposits to reserve at least 10 percent of their respective amount. Smaller institutions (with deposits between $16.3 and $124.2 million) are only required to keep three percent of deposits on reserve.

Essentially, these institutions are putting your money to work for themselves by loaning it out, or doing God-knows-what else with it, while providing you a fractional amount of the interest payout.

What's more, it's estimated that only eight percent of the total money in circulation in the world is in physical cash. The vast majority is represented digitally, in the form of ones and zeros. The implication here is that, in the event of a national electrical power grid crash, you could be left with nothing. If it’s not something you can physically possess and hold in your hand, you don’t really own it. This principle is applicable to other methods for storing savings as well, particularly cryptocurrency.

Cryptocurrency

While the Steem community is, in general, very familiar with cryptocurrencies like Bitcoin and Ethereum, my view on cryptos may be a mild departure from the popular opinion found on Steem forums.

Many alt-thinkers and self-proclaimed anarchists champion the use of cryptocurrencies, mainly Bitcoin, as a way to loosen the stranglehold these banking institutions have on society's finances. The primary advantage of Bitcoin for the conscious consumer is its use of [ blockchain ]( https://en.m.wikipedia.org/wiki/Blockchain ] technology, which utilizes a community of individuals working together to approve payments made with the cryptocurrency in a collaborative, digital ledger. In general terms, what makes Bitcoin so valuable is that it has a stable money supply, unlike the US dollar (which was tied to the price of gold until the early 1970s). There are only — and will ever only be — 21 million Bitcoins in existence. This is by design of the pseudonymous creator, Satoshi Nakamoto, who also developed the first blockchain database.

On the flip side, as the technology has become more accepted in the mainstream, and its potential as a currency of the future has grown more realistic, many private and public entities have begun to develop there own form of digital currency. For example, you’ve probably heard about the future launch of Facebook’s crypocurrency, Libra. These currencies, when backed by US dollars and a bank, are known as “stablecoins”, as they are seemingly tied to something that has monetary value.

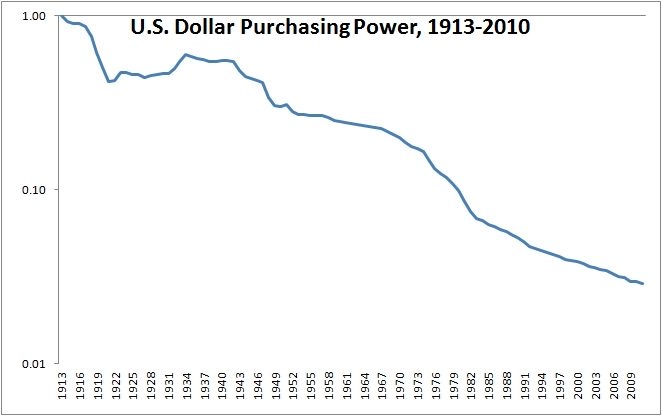

However, it is inaccurate to call these cryptos “stable” in the sense that the US dollar is anything but. While it may be stable in the sense that quite often it rises against other national currencies or the euro, in fact, it is constantly devaluing; the purchasing power of the US dollar has been on a straight downward trajectory over the past century-plus.

The regulation of stablecoins or other cryptocurrencies by governments or corporations, is antithetical to the premise of Bitcoin, as it seeks to keep financial markets privatized in the the hands of these institutions, rather than the people.

Additionally, many of the same pitfalls of digital currency apply to cryptos. You aren‘t physically in possession of the asset, and it is just as susceptible to go up in smoke in the event of a power-grid collapse.

What’s more, while allocating a portion of your financial portfolio to cryptocurrencies like Bitcoin can be a good hedge against a stock market correction or US dollar crash, the risks and volatility of cryptocurrency should be seen as major drawbacks, and prevent the individual from viewing these assets as viable investments and concentrating too high a percentage of their money there.

Securities (Stocks and Index Funds)

A lot of individuals choose to invest their income in securities, i.e., stocks and bonds. Many large employers offer automatic contribution programs for employees, such as a 401k or Roth IRA, which, when opted for, allocate a certain percentage of the employee’s weekly or bi-monthly earnings to be added to their account. However, you will be taxed when making contributions to any of these employee-savings plans, except for a 401k. Essentially, a 401(k) is a pretax savings account. When you invest in a traditional 401(k), your contributions go in before they're taxed, which makes your taxable income lower. This approach is the most logical choice for individuals seeking to minimize government fees and maximize their savings. With Roth IRAs, you pay taxes upfront, and qualified withdrawals are tax-free for both contributions and earnings.

Often the employee has little investing knowledge, so they will opt to buy shares of an index fund or exchange-traded fund (ETF), rather than those of an individual company with their contributions. Index funds and ETFs are funds that represent a theoretical segment of the stock market, and could be based on company size, industry or geographical location, among other parameters. However, since in this case the companies are selected for you, they individual lacks the ability to select particular companies on their own specifications, and there is a solid chance you are funding companies that engage in amoral business practices or crony capitalism, while it may not be apparent on the surface.

For the discerning, socially-conscious investor, there are ESG-based (environmental, social, and governance) index funds and ETFs, which theoretically select only the most socially and environmentally responsible companies to be included. Rather than using the age-old Friedman doctrine of investing, which surmises that companies' only responsibility is to maximize shareholder value, ESG-focused companies seek rather to maximize value for all stakeholders. This includes all entities which the company should have a vested interest in, including employees, the environment, suppliers, customers and communities.

There are several resources online which individuals can use to screen companies and ETFs based on their social and environmental responsibility merits, such as the Forbes Just 100 list of the most ESG-conscious publicly-traded corporations, or the company As You Sow , which offers online tools you can use to plug in a given ETF or mutual fund to see if it invested in companies that hurt deforestation, or don't have a lot of gender equity, for example. Theoretically, this would be a great approach for any individual investor to use to prevent themselves from investing in companies that don't align with their values. However, upon further investigation, these resources are not all they are cracked up to be.

However, taking one look at the Just 100 list, one can determine the list, constructed by Forbes, is less than authentic. It has clearly been cherry-picked, and maybe even sponsored by the companies on the list. For example, I find it shocking that Alphabet – the parent company of Google – is the the third company on the list, considering it had thousands of employees walk out of its offices in 2018 after allegations of a "destructive culture" that condones sexual misconduct, discrimination and racism, and the issue seems to be ongoing based on recent allegations.. Also in 2018, it was reported that the company kept silent about a male executive who was accused of sexual harassment , and awarded him a $90 million severance bonus when he was let go.

Other corporations cracking the top 50 are Apple and Nike, who both have a long history of unethical labor practices overseas .

Then there's companies making the list like Johnson & Johnson and Dow Dupont , whose products have been proven to contain toxic chemicals , unbeknownst to consumers or the FDA and USDA. Most recently, Johnson & Johnson has been caught up in a class-action lawsuit regarding trace amounts of asbestos in its baby powder products, among other lawsuits .

Contrary to what we, the public, are led to believe, these companies seemingly are putting shareholder value, i.e., the maximization of profit, above the interests of their stakeholders.

On a different note, what's ironic is how these assets (stocks, ETFs and index funds) are referred to in finance as "securities”. Investing in index funds or ETFs over individual companies is a great way to reduce the amount of volatility in the share price as they provide diversification for the investor, but there is still the likelihood your invested capital may decrease, especially considering the current, rich valuation of the US stock market. More importantly, there is even the chance that in the future, they could be taken from you, or vanish altogether.

Owning shares — of both an individual company or in index fund — is not tangible ownership, as mentioned previously. The stock is not something you can physically hold in your hand. Traditional brokers provide you a piece of paper as a type of title or receipt when you purchase. Owning shares through digital stock-trading platforms — which have gained popularity in the last few years, especially with millennials — such as Robinhood or Charles Schwab, are even less tangible, as your receipts or other proof of ownership are strictly digital.

Precious Metals (Gold and Silver)

One form of currency that does provide security, however, is precious metals. The conscious consumer's preferred form of currency for storing wealth should be metals, namely gold and silver. Though not very high in terms of liquidity, precious metals provide security in the sense that their value will not collapse to zero. In fact, owning gold and silver is the ultimate hedge against any future economic meltdown or mass electrical grid crash that may occur.

Though the rate of appreciation of precious metals' value is lower than most of the other forms of currency laid out here, metal prices still have appreciated significantly over the past 50 or so years, and for the most part, at a more consistent rate than the stock market. As of this writing, the price of gold is up more than 2,200 percent since 1973.

That being said, the conscious consumer's primary motivation should not be to "make a profit". The main concern with respect to financial holdings is to have guaranteed security, and financial independence from the controlling system. Precious metals provide both.

Additionally, the lack of liquidity for gold and silver can actually be seen as a benefit rather than a drawback, as difficulty converting to cash or inability for use in everyday purchases will deter frivolous spending.

There are many websites you can use to buy precious metals online, like JMBullion.com , and physical stores selling gold and silver can be found in most large or mid-sized cities around the world. My recommendation is to buy a little at a time from a variety of dealers, to ensure you don’t get taken advantage of and aren't left stuck with a bunch of counterfeit coins or bars.

Diversification is a good thing in most walks of life, and it makes sense to dedicate a little of your portfolio to most or all of these assets. But when it comes to financial health, security, stability, self-preservation and minimal contribution to unethical practices is what the conscious consumer should strive for. Given these criteria, the most logical location for storing the bulk of one's net worth is precious metals.