In his revealing book and documentary "The Great Taking," David Rogers Webb uncovers a decades-long transformation of global securities reglementations that has fundamentally altered the nature of financial ownership. Webb's work demonstrates his deep understanding of complex financial systems and regulatory frameworks, allowing him to piece together a story of systematic legal subversion that has largely gone unnoticed by the general public. His analysis draws on extensive documentation from regulatory bodies, central banks, and financial institutions.

N.B.: «The Great Taking», both as a book and a documentary, is available free of charge from: https://thegreattaking.com/

Let’s precise from the get go that the concept of «securities» here doesn’t refer to stocks and bonds only, but also to investment funds, savings plans, pension funds,… in short: any contractual asset.

The Dematerialization Strategy

Webb traces the origins of this transformation to the late 1960s, when the process of securities dematerialization began in the United States. What appeared to be a simple technological modernization - moving from physical stock certificates to electronic book-entry systems – was actually a carefully orchestrated shift in ownership rights. Notably, he points out that the CIA was involved in this initiative, with William Dentzer Jr., a career CIA operative, appointed as the first Chairman and CEO of the newly formed Depository Trust Corp. (DTC), that he’ll lead for twenty-two years (1).

The official justification for dematerialization was what was called the "paperwork crisis" of the 1960s, when the burden of handling physical stock certificates allegedly became overwhelming. However, the author questions this narrative, noting that markets continued to function with physical certificates for many years after, even as trading volumes increased.

«When we had paper certificates, the public was absolutely bullet-proof from insolvency. [Those certificates] couldn’t be transferred for use as collateral by another party» (2)

1994: from property owners to «entitlement holders»

The next key innovation was the creation of the "security entitlement" concept, which replaced direct ownership of securities with a contractual claim against an intermediary. This change was gradually implemented through modifications to the Uniform Commercial Code (UCC) in all 50 U.S. States – State by State, so that such a huge shift would never be tackled by the Congress itself, at the Federal level. Webb cites a crucial exchange between the European Union's Legal Certainty Group and the Federal Reserve Bank of New York that reveals the fundamental changes in securities ownership. The Deputy General Counsel for the Federal Reserve Bank of New York explicitly confirmed that under the revised Uniform Commercial Code (UCC):

1. Securities are held in "fungible bulk" with no specifically identifiable shares owned by individuals, hence no rights from securities holders to particular securities (even if those same securities are held in a segregated fashion in the brokers-dealers books and apps, like Robinhood’s, the brokers themselves have no say at the upper level);

2. Account holders receive only a pro-rata share of residual assets in case of intermediary insolvency;

3. Recovery of specific securities ("re-vindication") is prohibited;

4. Account providers can legally use pooled securities – our stocks, bonds, etc. - as their collateral;

5. Secured creditors with «control» have priority claim over account holders (3) – in plain English: the big banks have priority over us, so that they’ll vacuum-clean our assets.

European Harmonization towards Financial Totalitarianism

Webb documents how this U.S. model was then exported globally, particularly to the European Union. The process, euphemistically called "harmonization," involved significant pressure on European nations to conform to the U.S. approach. This was achieved through various mechanisms, among which:

• The 2002 EU Financial Collateral Directive [2002/47/EC]

• The 2014 Central Securities Depository Regulation (CSDR)

• The creation of International Central Securities Depositories (ICSDs)

An especially striking example of this imposition are the Nordic countries. Sweden and Finland, which once had strong property rights protections for securities holders, saw their systems fundamentally altered after Euroclear acquired their central securities depositories in 2008. Following legal changes in 2014, Swedish citizens can no longer hold even their own government bonds with direct property rights...

The Role of Central Clearing Parties in Collateral Management

At the heart of this new system are the Central Clearing Parties (CCPs – pun probably intended), which have become the focal points of systemic risk in the global financial system. Webb raises serious concerns about their capitalization levels. For instance, he notes that the Depository Trust & Clearing Corporation (DTCC), which operates the main U.S. CCPs, had total shareholder equity of only $3.5 billion as of March 2023 (4) - a remarkably small amount given the scale of markets it supports, the derivatives markets worldwide being often estimated at over $1 quadrillion (1,000 trillion dollars). (5)

The author argues that this undercapitalization is not accidental but rather by design. He points to statements from DTCC officials indicating that they are actively planning for potential CCP failures and have pre-funded arrangements to start new CCPs if necessary.

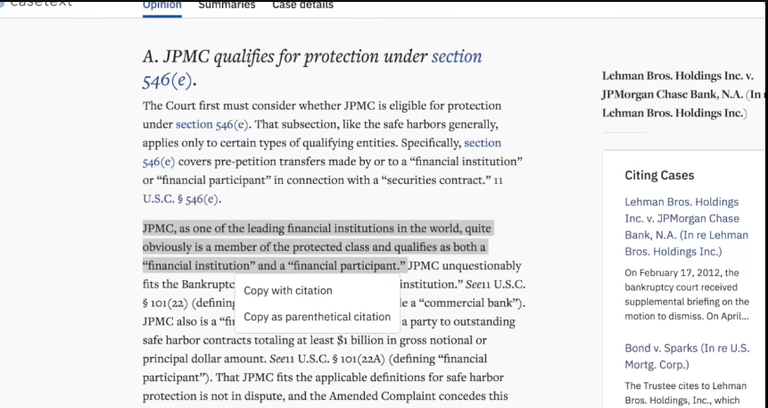

But who controls these Central Clearing Parties, are you maybe asking yourselves? Well, the select «secured creditors» that the Southern District of New York judge called the «protected class» during the 2012 Lehman Brothers bankruptcy procedure (6): a handful of banks. Although David Webb does not explicitly identify or list the specific "secured creditors" he refers to in the book, we can confidently turn our eyes to the 5 banks that are responsible up to 95% for the creation of the derivatives complex: JPMorgan Chase & Co., Bank of America Corporation, CitiGroup, Goldman Sachs Group, Inc. and Morgan Stanley.

The Implications

The significance of this progressive and methodic legal subversion becomes clear when considering its potential consequences in a financial crisis. Under the current system, client assets held in custodial accounts, pension plans, and investment funds are effectively being used as collateral underpinning the massive derivatives complex. In the event of a major market disruption, Webb warns that these assets could be swept up by secured creditors with priority claims, leaving nominal owners – i.e. us - with only pro-rata claims against insolvent intermediaries. The author stresses that:

«They’re saying that there will not be enough cash in government bonds to cover what is coming (...) In 2013, in a Bank for International Settlements paper showing the plumbing for all of this (7), they discuss «collateral transformation», which means using other types of securities, other than government bonds. (…). Their flow charts show the collateral going from the collateral givers to the collateral takers, and they discuss very clearly that that will happen on an automated basis, particularly in a crisis, without human intervention» (8).

While reading David Webb’s book, or watching his documentary, we unveil step by step how the financial world’s reality is the exact opposite of what we’ve heard thousands of times from the most famous market analysts: at their core, the high risk assets are all the ones deemed to be «refuges», like sovereign bonds or ETF’s shares, and the secure ones in times of real trouble are the assets that use to be tagged as «speculative», like Bitcoin.

Conclusion

The significance of Webb's work lies not just in documenting the carefully orchestrated shift in ownership rights through legal and regulatory changes spanning decades, but in highlighting their potential consequences during the next financial crisis.

The only assets to escape that coming «Great Taking», and that all citizens should focus on, are – for now – the physical ones we have paid for in their entirety (land, houses, precious metals in their physical form,…) and the digital ones that are under our direct custody – meaning, in the case of cryptocurrencies, the ones we access to through non custodial wallets, i.e. via our private keys & seed phrases.

«The Great Taking»’s content is a testament to the urgency of owning self-custodied & non KYC’d assets.

Notes:

(1) Webb, «The Great Taking», Chapter II: Dematerialization

(2) David Webb’s quote from the video: The Great Taking: How Banks Could Legally Seize Your Assets | Counterpoint 13 – 06:27

(3) Webb, «The Great Taking», Chapter III: Security Entitlement

(4) Webb, «The Great Taking», Chapter VII: Central Clearing Parties

(7) "Asset Encumbrance, Financial Reform and the Demand for Collateral Assets", Committee on the Global Financial System, Bank for International Settlements (BIS)

(8) David Webb’s quote from the video: The Great Taking: How Banks Could Legally Seize Your Assets | Counterpoint 13 –

(5) https://www.investopedia.com/ask/answers/052715/how-big-derivatives-market.asp

(6) «The Great Taking – Documentary», 25:45, https://inv.nadeko.net/watch?v=dk3AVceraTI

Images sources:

- https://alternativefinance.com.br/wiki/blog/portfolio/dtcc-depository-trust-clearing-corporation/

- «The Great Taking – Documentary», https://inv.nadeko.net/watch?v=dk3AVceraTI

Posted Using INLEO