Image Source – Modified

The negative interest rate is a very recent phenomenon. The European central bank (ECB) adopted negative interest rate in 2014 to address the eurozone crisis. They made deposit rate (-) 0.1% that time. At present, ECB has (-) 0.5% interest rate and this is the lowest interest rate of their history. The Bank of Japan (BoJ) adopted zero interest rate in 1999 and they have maintained a negative interest rate since 2016. Recently there has been news that the Bank of England will follow many other central banks to launch negative interest rate. A few days back the UK sold a bond with negative yield for the first time in their history. Trump also tweeted weeks back that the US should accept the ‘gift’ of negative interest rate and join other countries. Trump has been an advocate of negative rate throughout his presidency. In March, Fed slashed interest rate to bring it near zero to combat with the coronavirus pandemic.

So, is the negative rate a gift?

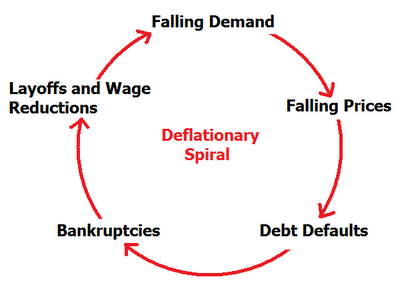

Negative interest rate looks very crazy on paper. Imagine that, you are lending 100$ to someone for one year with (-) 2% interest rate. That means the borrower needs to pay you back only 98$ after one year in a very simplified calculation. There is also the risk of not getting the money if the borrower defaults. Obviously desperate measure! It is not a gift. It is basically a tool of the central banks to boost the economy. During economic downfall, people start hoarding money and spending in the economy get reduced. Demand decreases in the economy and as a result inflation gets reduced. If demand falls dramatically, deflation gets started. The negative interest rate helps to fight deflation. As holding money becomes costly, people start spending the money into the economy and the economy gets boosted by the money flow. This is the basic mechanism. It can be used as a short term tool. If you think it to use for the long term, there are serious implications.

Image Source – Negative interest rate is widely applied when the central banks fear about deflationary spiral

How does it affect me and you?

When the central bank charges negative interest rate, your banks are encouraged to not park the money with the central bank and lend more. When the banks start lending aggressively, the interest rate drops further due to the market dynamics. Yes, you might be able to grab a loan from your bank with nominal, zero or negative interest rate too. Obviously in that scenario, your deposit with the bank has no scope to earn interest rate. Most probably your bank will also charge a storage fee for parking money with them. In Europe, some depositors have started to hold money in the bank vaults rather than depositing the money in their account to avoid negative rates. So it creates a very strange situation.

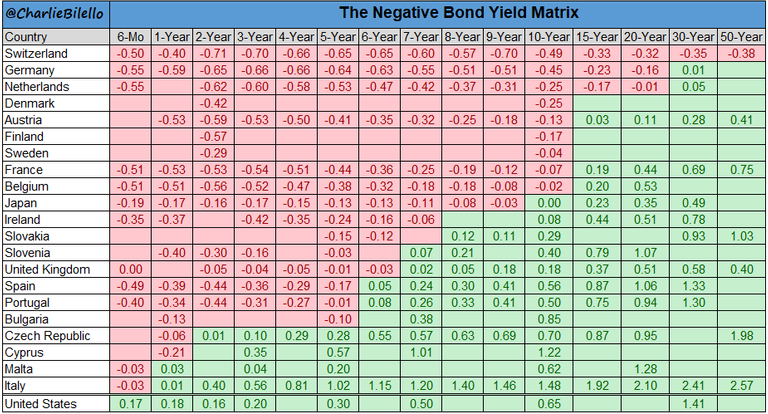

Image Source – The negative bond yield matrix

Gonna be a long story!

ECB does not want the euro to be strong. The negative interest rate was brought to bring the euro value down. Europe’s perennial problem has been weak demand. A weak euro can stimulate the export demand and the corporates will be lured to expand outside. Even Trump hates strong dollar. The future consumption market lies outside America & Europe. A weak currency can help to capture that market. So the negative rates are here to stay. Be assured! The yield of the government bonds of several nations indicate that only.

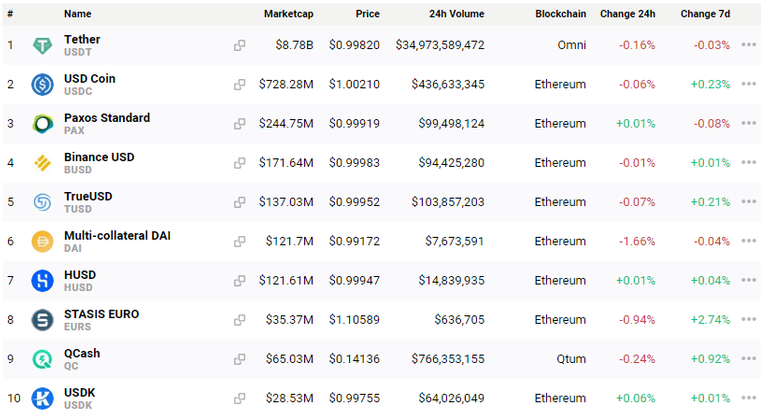

Image Source – Top 10 stablecoins

Oh your stablecoin!

Are you hoarding your stablecoin since a very long time? Some people hoard stablecoins to hedge against crypto market volatility. Recent stablecoin minting had a role behind Bitcoin pump. Total stablecoin market cap is currently $10.53 billion. USDT from Tether is the largest stablecoin. Currently it has surpassed XRP to attain the number 3 slot in the coinmarketcap. Stablecoin demands are very high. Stablecoins often act as an entry bridge for an investor to enter into crypto. Tether has been minting USDT in a crazy manner since last a few years. There have been numerous scams related to stablecoins. USDT is controversy’s favourite child. The asset backing of tether has always remained suspicious. But let’s consider for a moment that all stablecoins are transparent. Now these stablecoin makers lock dollar in the bank and issue stablecoin against them. Almost all stablecoins are pegged to the dollar. What happens to your stablecoin’s value when the bank starts charging storage charge to these stablecoin makers? The stablecoin makers will be forced to pass on some fees to you for hoarding their stablecoin. I foresee a collapse in the stablecoin game in that case.

DAI/USD 90 days chart from Coingecko – The pressure on DAI is visible

COVID-19 is here to stay. We’ll have to live with that. The pandemic has already affected the economies all over the world and it is expected that it’ll affect more. The negative interest rates will be more widely used till the time the scope of occurrence of deflationary spiral remains. The negative rates are paradoxical in nature. This uncharted monetary policy’s proper outcome is never known. The pressure on the banks will surely be enhanced. Your stablecoin is going to be affected logically. MakerDao introduced USDC as collateral with zero stability fee some months back. DAI used to trade far above dollar although it was pegged to the dollar. Now DAI is trading with the value of almost 1$. DAI stability rate is decided by MakerDAO voting and it affects the price of DAI. The pressure on DAI is visible. I don’t hold stablecoin for a long time. There is basically no reason to trust centralized stablecoins. These are worse than your bank deposit and probable scams can pop up any time as transparency is a doubtful factor. DAI is any day a better option if you decide to hold stablecoin. At least it is fully transparent, auditable and decentralized. DAI uses crypto collaterals, so it does not need any bank to deposit the collateral and it is not going to be affected by negative interest rate. I found the news funny when MakerDao included centralized stablecoin USDC as collateral but due to zero stability fee on USDC, its usage is very less in DeFi. That has saved DAI. The negative interest rate party is not going to be over soon. Be cautious about stablecoins and trade wisely.

Cheers!

[paragism]

Posted Using LeoFinance

#posh