I’m forever blowing bubbles,

Pretty bubbles in the air,

They fly so high, nearly reach the sky,

Then like my dreams they fade and die

John Kellette, Jaan Kenbrovin 1918

Hardly a day goes by without a story that financial markets are in “bubble” territory. Stock markets around the world, including the FTSE All-Share, are at record highs and bond yields are at record lows. The former means that valuations are at the upper end of historic ranges. The latter has meant that many unusual things can be sold to investors anxious for yield. Recent examples include a 100-year bond with a coupon of just 2.1% that raised €2.5 billion for Austria. Possibly a better risk than the three 100-year bonds issued by Mexico in recent years but at least the Mexican government prints its own currency.

Despite the money that has been made by those who have stayed invested in bonds and/or equities in recent years, there is little sign of euphoria. Rather in our experience, investors remain nervous and many choose to hold significant amounts of cash.

This appears to be a conservative strategy but in fact it is a rather risky one. The obvious problem is that with rates at record lows you receive virtually no interest on your capital.

But the bigger problem is that with inflation running well above the level of interest rates the supposedly conservative strategy of putting money in the bank is actually destroying your purchasing power at a rather alarming rate.

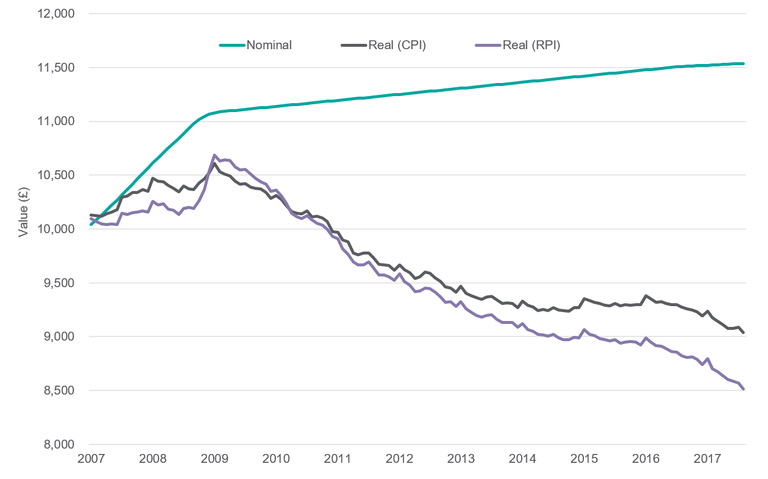

The chart below shows what has happened to £10,000 deposited in a bank over the last decade. We assume the deposit is receiving interest at the level of the Bank Rate set by the Bank of England.

The fate of £10,000 deposited in a bank at the end of 2006

Source: Bloomberg, Highcharts, Waverton – data from 01.01.07 to 31.08.17

The green line shows your original £10,000 and increases it by the bank rate each month. It would today be worth £11,539. This looks pretty reasonable. You have 15% more money than you had at the end of 2006 and you have taken no risk.

But inflation has not been as low as interest rates have been. In fact despite all the talk about “deflation” in recent years, UK CPI (Consumer Price Index) has averaged 2.3% and RPI (Retail Price Index) has averaged 2.9% since January 2007. Your portfolio has only been growing by 1.4% per annum

As inflation has been higher than the interest you have been receiving, your purchasing power has been declining. The black and purple lines in the chart show the impact over time of this problem. The black line shows what your £10,000 is worth after adding the interest you receive and then taking into account CPI. The purple line shows the same but taking into account RPI.

The bottom line is that the £10,000 you started with today buys just £9,037 thanks to CPI and an even worse £8,514 thanks to RPI.

So by putting money in the bank you have ended up reducing the purchasing power of your capital by between -10% and -15%.

If your wealth manager had reduced the purchasing power of your capital by that amount over the last decade you would not be happy. You might want to write to the Bank of England (BoE) about what they have done to you.

Even with the BoE likely to raise interest rates in November it will likely take a long time before the bank rate gets above the inflation rate. Consequently this trend of real capital loss from holding cash will continue for potentially years.

While we are conscious that financial assets have had a good run and that there are fewer opportunities to find attractively valued investments, we continue to dedicate our resources to finding such opportunities.

We expect a diversified global equity portfolio, or a balanced portfolio of equities, corporate credit and government bonds, to continue to provide investors with capital growth in real terms. In fact such portfolios may be less risky to your financial well-being than sticking your money in the bank.

By William Dinning

Head of Investment Strategy and Communication

RISK WARNINGS

The views and opinions expressed are the views of Waverton Investment Management Limited and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material(s) have been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

Changes in rates of exchange may have an adverse effect on the value, price or income of an investment.

Past performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise. Capital security is not guaranteed

The information relating to ‘yield’ is for indicative purposes only. You should note that yields on investments may fall or rise dependent on the performance of the underlying investment and more specifically the performance of the financial markets. As such, no warranty can be given that the expressed yields will consistently attain such levels over any given period.

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://ceylontoday.lk/print20170401CT20170630.php?id=37121