In this article, we explore the complex tax issues that cryptocurrency miners will face for this filing season.

Is cryptocurrency earned from mining taxable? Crypto Tax Blog Part III, Section A

IRS Cryptocurrency Rules

The IRS provides limited guidance on the U.S. income taxation of cryptocurrency in Notice 2014-21. For U.S. income tax purposes, “convertible virtual currency” (CVC) is treated as property for tax purposes. Convertible virtual currency means Bitcoin any other virtual currency that can be:

(1) Digitally traded between users and

(2) Purchased (and sold/exchanged) for U.S. Dollars (or other currencies including virtual currency).

More information can be found in the Part I-A blog:

Mining – Tax Event #1

The IRS declared in its crypto notice that mining income is taxable gross receipts for purposes of U.S. income tax. The fair market value of virtual currency is includible in gross income when it is successfully mined (Notice 2014-21, Q&A 8). Fair market value must be calculated in a consistent and reasonable manner (Q&A 5). An example could be the exchange which a miner transacts with if it is liquid. How this calculation would actually work is in an example down below.

Furthermore, mining income could be considered to be conducted under a trade or business and thus may be subject to self-employment tax (Q&A 9).

All is not lost, because deductions are claimed against the income, otherwise the profitability of mining would be significantly reduced for U.S. tax payers, as applying a tax just to the currency earned without regard to deductions would be devastating.

Deductions

Deduction vs. Hobby

Generally, in assessing tax consequences of mining, this will require a taxpayer to determine if mining is a trade or business or is a hobby. Generally, if a taxpayers has a profit in 3 out of 5 tax years (ending with the year analyzed), the activity is “for profit” and thus not a hobby. However, it is up to the taxpayer to determine whether mining is a trade/business or a hobby. A tax advisor should be contacted to help assess the trade/business vs. hobby assessment.

Why is this important? Under Code Section 162, ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business are deductible. However, under Code Section 183, expenses incurred related to an activity that is not engaged for profit (a hobby) are deductible only to the extent of the income. This generally results in deductions that are subject to a 2% miscellaneous itemized deduction limit (substantially limited).

Expenses Miners Incur – The Tangled Web of a “Home Office

The examples of expenses miners incur are:

- Cost of hardware to mine (ASIC miner, GPU rigs, cost of computer)

- Electricity cost

- Miner pool fees an exchange fees.

For a small-time miner who made a purchase of an ASIC, the problem is the cost of electricity is usually tied to an individual miner’s place of residence. The electricity generated from the activity is with the residential electricity bill. The IRS permits a deduction for expenses related to a living unit, but only if the expenses are connected to a taxpayer’s trade or business. This is known as code section 280A. A taxpayer cannot take a home office deduction with respect to a hobby. For a taxpayer that has a full time job but mines cryptocurrency off to the side, as long the mining activity is a true “trade or business”, the home office deduction is permissible. A tax advisor should be contacted to help assess the home office deduction and ability to take a write-off for electricity.

It should also be noted that the cost of mining equipment may be subject to depreciation provisions, although equipment is relatively cheap relative to the Section 179 and bonus depreciation (168(K)) provisions, meaning a significant amount can be written off in the first year.

Disposition of Mined Currency– Tax Event #2

It should be noted that the subsequent sale/exchange of mined cryptocurrency results in a second taxable event (unless like kind exchange applies). The character of this second gain/loss could be ordinary or capital, depending on whether the mined cryptocurrency is a capital asset in the hands of the miner (see Q&A 7 & 7).

Inventory is an example of an asset that is not a capital asset in the hands of a taxpayer. So that leads us to wonder, is mined cryptocurrency an ordinary income asset, as it related to the miner’s activity of engaging in profit. It might be on the burden of a taxpayer to show their habitual treatment of mined bitcoin (i.e. immediately trading into fiat currency versus holding as an investment).

Example

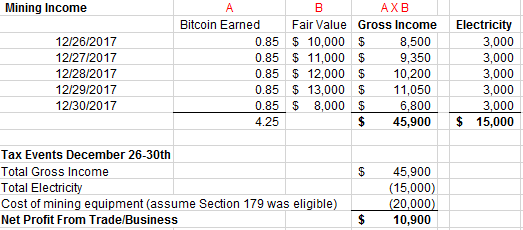

Crypto Bro purchased an ASIC miner for $20,000 USD, which was delivered to him on December 25, 2017. Crypto Bro used an ASIC miner in order to mine Bitcoin. Crypto bro intends to operate his mining activity as a trade or business. At the current difficulty, the miner generates 0.85 Bitcoin per day. He mined on December 26, 27, 28, 29 and 30th. The fair market value of the mined Bitcoin were $10,000 USD on December 26, $11,000 USD on December 27, $12,000 USD on December 28, $13,000 USD on 29 and $8,000 USD on December 30. He skipped December 31, 2017. Every day, the electricity cost (calculated by his tax advisor) is $3,000 USD. On December 31, 2018, Crypto Bro sold all of his Bitcoin that was mined in 2017 for $100,000, when the holding period was long-term. Crypto Bro is in the 25% marginal bracket (15% long-term capital gain rate).

Below is a general estimate of Crypto Bro’s income from mining

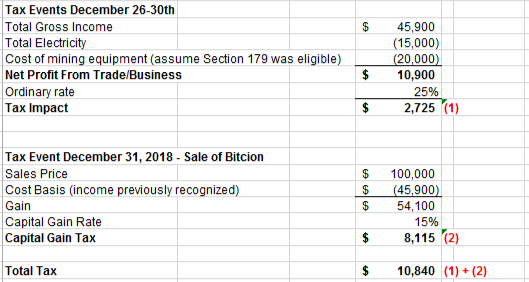

If Crytpo Bro’s Mined Currency is a capital asset, the tax is as follows

The first layer of tax is recognized on the 2017 tax return, the year the coins were successfully mined. The second layer of tax applies to the 2018 tax return (year when the Bitcoin is disposed of). Amounts above are totaled but span two tax return years.

NOTE: Calculation ignores Self-Employment Tax Impact which would also apply to increase the ordinary rate.

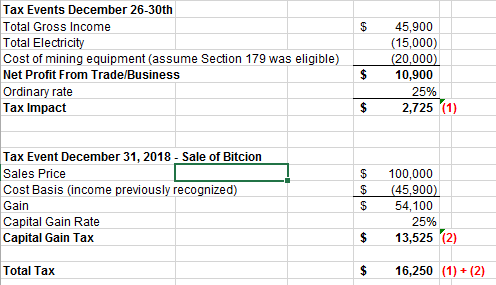

If Crytpo Bro’s Mined Currency is an ordinary income asset, the tax is as follows

The first layer of tax is recognized on the 2017 tax return, the year the coins were successfully mined. The second layer of tax applies to the 2018 tax return (year when the Bitcoin is disposed of). Amounts above are totaled but span two tax return years.

NOTE: Calculation ignores Self-Employment Tax Impact which would also apply to increase the ordinary rate.

The difference between the two scenarios

Takeaway

Cryptocurrency taxation is complex, and there are even more complex considerations for miners. Do you have any questions or thoughts of other challenges that miners may face related to U.S. income taxation? Feel free to post them here, however this is not personal tax advice, so it is also recommended you consult your tax advisor.

Note: Upcoming tax reform could result in changes to tax law as discussed in this article.

Disclaimer: This series contains general discussion of U.S. taxes in a developing and unclear area of tax law. As always, you should consult your own tax advisor in your jurisdiction to determine your specific situation as this is not personal advice; and consider any future guidance by the Congress/IRS after the date of this article. Under Circular 230 to the extent it applies, this article cannot be used or relied on to avoid any tax or penalties in the U.S., its States or any other jurisdictions. Last, this article does not create a client relationship between author and reader.

Picture Credit

Calculations: Me using Microsoft Excel

Cover Picture: https://pixabay.com/en/users/ArtsyBee-462611/

All is not lost if you end up paying the Social Security/Medicaid taxes from self-employment (due to making a profit of $400 or more). Half of it can be deducted from your income for income taxes. (The actual math is a bit complex.) Also, these are legit Social Security taxes, meaning you do get SS credits for paying them. This probably doesn't matter unless you don't have a job elsewhere. But hey, if you quit your job to work on bitmining full time, there you go.

If, as quite possible, your bitmining is unprofitable, you could theoretically use it to reduce your income taxes from another job or business. If you can convince the IRS it's not just a tax shelter disguised as a business. See: the hobby loss rule.

If you are planning to go into business as a bitminer, please research Section 179, since it will probably make your life much easier. Or, as @cryptotax says, consult a tax adviser on it.

Disclaimer: I'm not a tax professional, but I am a small businessman, so I learned this stuff.

Thanks for the thoughtful post as always. Agree, the 1/2 self employment is an "adjustment" to AGI. I kept it out of the example because it would muddy up the charts.

Also agree on Section 179. Depending on the time of the year of the purchase, it might be feasible to forgo 179 so establish a small positive profit for the trade/business argument or avoid hobby loss limitation (although I may have to double-check how the test and limit mechanically works). Planning with a tax adviser is best because other non-crypto related tax return activity should be considered in overall decision-making.

Today, I see the biggest grey areas are electricity deductions (i.e. how it is blended through home office / hobby rules) and and classification of mined crypto as (a) capital asset or (b) ordinary income asset.

Disclaimer: This is not tax advice (see general disclaimer for authored post above).

@steem-marketing has voted on behalf of @minnowpond. If you would like to recieve upvotes from minnowponds team on all your posts, simply FOLLOW @minnowpond.

To receive an BiggerUpvote send 0.5 SBD to @minnowpond with your posts url as the memo To receive an BiggerUpvote and a reSteem send 1.25SBD to @minnowpond with your posts url as the memo To receive an upvote send 0.25 SBD to @minnowpond with your posts url as the memo To receive an reSteem send 0.75 SBD to @minnowpond with your posts url as the memo To receive an upvote and a reSteem send 1.00SBD to @minnowpond with your posts url as the memo@OriginalWorks

To call @OriginalWorks, simply reply to any post with @originalworks or !originalworks in your message!

Of course, #taxationistheft

Since bitcoin isn't backed by anything except market psychology, is it wrong to say the fair market value of bitcoin is 0?

If on Jan 1 2018 bitcoin is worth 10k, but by december 31rst 2018 it is worth $5-do we still have to pay taxes at the 10k rate?

Good question. I added more information above regarding fair market value.

I don't follow your second question. Are you referring to my example in the article, re-worked if the price declined and the sale resulted in a loss? I can make another post with that example if there is demand for it.

Yeah i am basically using your example-different dates. Except instead of selling, they are held.

It seems the fair market values you are using are from the day that they are mined. Let's say we go 364 days with bitcoin at 10k+ [and we hodl], and on day 365 [end of the year] the proverbial s*** hits the fan and it is worth nothing. That is, For convenience, Let say the reported 10.9k profit under their accounting schemes is in reality a loss of about 35k. Does the IRS expect you to pay them $2500 in taxes under their accounting scheme.

Good question. In my example in the post, the first layer of tax is recognized on the 2017 tax return, the year the coins were successfully mined. The second layer of tax applies to the 2018 tax return (year when the Bitcoin is disposed of). Had the value decreased in 2018 to $1.00 on 12/31/2018 and sold at a 100% loss (instead of $100,000 I used in example), taxpayer would have still had income in year 2017 and a loss in 2018. However if the loss is capital loss, it may be limited to $3,000 per year under US individual income tax law.

Of course same with dislaimer above, this is not personal tax advice, cannot be used to avoid penalties, and is subject to new legislation after the date of this post.

@mrainp420 has voted on behalf of @minnowpond. If you would like to recieve upvotes from minnowponds team on all your posts, simply FOLLOW @minnowpond.

To receive an BiggerUpvote send 0.5 SBD to @minnowpond with your posts url as the memo To receive an BiggerUpvote and a reSteem send 1.25SBD to @minnowpond with your posts url as the memo To receive an upvote send 0.25 SBD to @minnowpond with your posts url as the memo To receive an reSteem send 0.75 SBD to @minnowpond with your posts url as the memo To receive an upvote and a reSteem send 1.00SBD to @minnowpond with your posts url as the memohere an easy Way of mining with Google Chrome:

Bitcoin-Mining

Give 5$ and Get5$, Join Uber for Cryptocurrency Referral Program By Coinswitch.co.

Check out more on coinswitch.co/referral