Interest rate expectations: drivers of foreign exchange rate

Future interest rates are expected to be higher than headline interest rates.

If a country has high interest rates, but without further growth expectations, the currency can still fall.

If a country's interest rates are low but are expected to rise over time, its currency can still appreciate.

It is easy for foreign exchange traders to understand why investors are shifting money from lower-yielding currencies and assets to higher-yielding assets and currencies. They may also think that a simple supply and demand mechanism are the cause of currency movement. However, this is only part of the story. Expectations for future interest rates to rise or cut interest rates are even more important than real interest rates themselves.

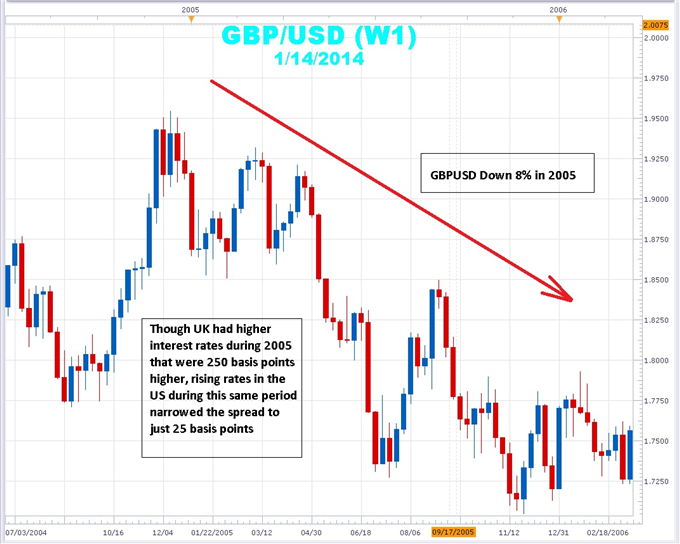

Learning foreign exchange: interest rate is expected to sink GBP/USD.

Interest rate expectations: drivers of foreign exchange rate

For example, interest rates in Britain range from 4.5 to 4.75%, much higher than that in the United States by 3.25%. Traditional wisdom will decide that the pound should appreciate against the US dollar over that time. However, as shown above, this is obviously not the case, because the pound fell against the US dollar. The reason is that the Federal Reserve will start tightening interest rate cycles. In early 2005, the 250 base point premium in Britain narrowed to just 25 basis points. The Fed raised interest rates from 3.25% in December 2004 to 6% in May.

If a central bank decides to raise interest rates one day and then says they can raise them in the foreseeable future, money can still be sold even if interest rates rise.

On the other hand, if a central bank starts raising interest rates sharply to curb inflation and inflation remains high, investors around the world realize that there is no way out for interest rates to rise. The currency may continue to appreciate as people anticipate the increase in interest rates.

Learning foreign exchange: NZD/USD interest rate rising trend

Interest rate expectations: drivers of foreign exchange rate

In the above example, as the Reserve Bank of New Zealand continued to raise interest rates, the NZDU dollar rose 57%. From 2002 to 2005, RBNZ raised interest rates from 4.75% to 7.25%, while the Fed raised them from 1.73% to 4.16% over the same period. Investors seeking higher returns earn NZD with lower yield dollars for higher yields. As a result, NZDU US dollar rose 57%.

If future interest rates are close to zero, investors will want to look elsewhere for a country where interest rates are rising. The market is a discount mechanism, which means favorable news, for example, the price hike has been raised. To continue to provide value, there must be signs that interest rates will continue to rise to justify the rise in money prices. Without any expected interest rate hikes, there is little incentive for new or past investors to enter.

On the other hand, extreme interest rate levels may change and turn interest rate expectations in the opposite direction, because investors think interest rates may return to the mean. Just as a rubber band extends to the extreme, rebounding, interest rates operate in a similar way. The highest U.S. interest rate in 1980 reached 3% in 1990 at 20%, and the very low interest rate after the global financial crisis could return to a much higher average than the current 3%. The bottom line is that foreign exchange traders must not only focus on the headline currencies, but also monitor interest rate expectations to keep themselves on the right side of the deal.

Sort: Trending