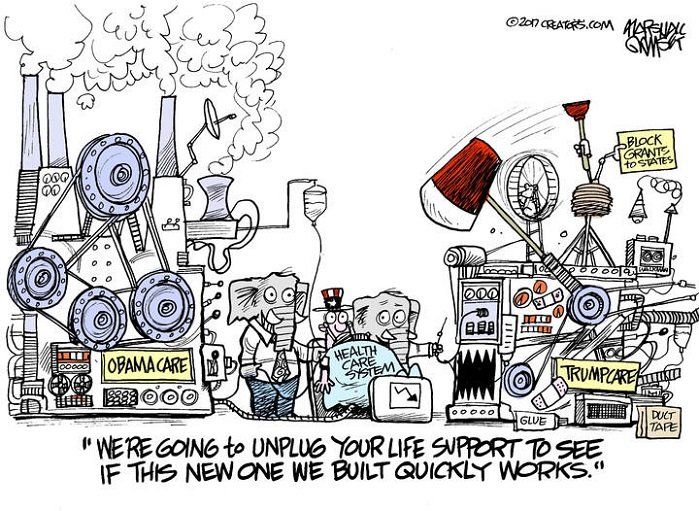

I’m sure many of you payed attention a couple weeks back when Trump succeeded in the first part of his plan to repeal Obamacare. However, I imagine an equal number of you missed the fine print when it comes to these systems. Lets analyze this together, and figure out how Trumpcare differs from Obamacare, and which is superior.

Obamacare 101

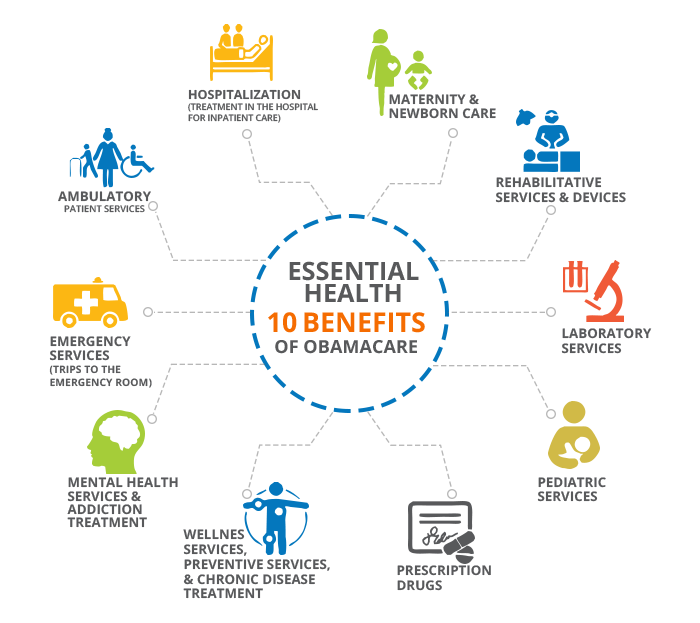

The Patient Protection and Affordable Care Act, better known as the Affordable Care Act (ACA), better known as Obamacare was signed into Law By President Obama on March 23, 2010. Its goal was to revolutionize the current system of medical care, allowing patients to have greater access to medical assistance, in a much more affordable framework than the one already existing. It did this mainly in one way: through insurance.

Previously, insurance companies could deny you coverage if you had some pre-existing health condition. After the Obamacare sweep, they no longer could. In fact, they could no longer ignore you in many of the situations in which they previously could: in case your income was too low, in case you were a kid who did not have coverage via your family, and in many others.

Also, you would now have subsidies in case your income was close to poverty levels. You could no longer delay in getting a health insurance until you were sick, nor could your company refuse to get you health insurance. Women private health also had greater coverage, among many other bureaucratic systems put in place to make it easier for everyone to be insured.

The Republican Party, against expectations, did not respond favorably to this. Many republicans argued against it, saying that Obamacare would increase health costs rampantly. Others simply opposed the idea of universal healthcare, which they felt the law represented. Others opposed that the law would force people to buy health insurance, which would represent coercion from the government. Lastly, the laws imposed on companies would cause a large decrease in personnel for most, which would cumulatively increase the deficit of the country.

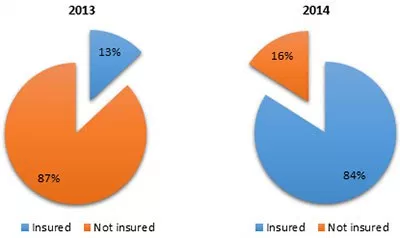

Despite that, come 2016, the numbers sang a different tune: throughout the implementation of Obamacare, from 2010 further, the annual healthcare costs decreased. Healthcare household spending by the middle class in 2016 was 8.9% of what it was in 2014.

While the net costs did indeed rise, and non-generic drug costs climbed, any employer difficulties were most likely due to the effects of the 2008 recession, and the number of insured people raised dramatically. By 2017, nearly 20 million people were insured thanks to Obamacare.

Then the repeal happened. Let’s explore what will come in the future.

Trumpcare 101

Republicans had targeted the ACA for repeal as early as the 2012 election, led by Mitt Romney. Trump renewed that sentiment in 2016, after many appeals throughout Obama’s second term had failed, vowing to “repeal and replace Obamacare with a new law”.

The new bill was worked on in secret by 13 Republican Senators, which by itself raised concerns on transparency. Dubbed the “American Health Care Act”, it introduced new age-based tax credits – meaning older people would have to pay more for insurance.

More meaningfully, it would remove several bureaucratic mechanisms of the ACA. Notably, the mandates that required an individual to insure himself, as well as many other taxes related to the former law.

In practical terms though, many experts have noted that it would reduce taxes for the wealthy, and overall increase premiums for older and poorer people, while reducing them for younger, wealthier, healthier people. In total, 24 million people would lose their health insurance by 2026, due to the eliminations of mandates.

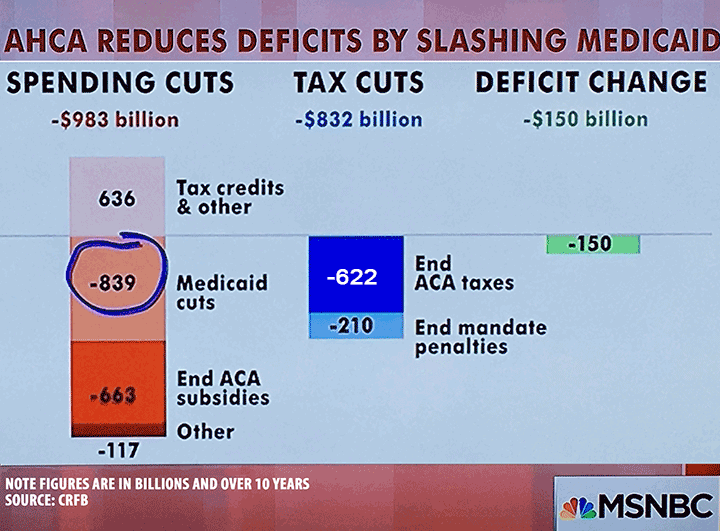

Its advantages lie mainly in deficit reduction. Compared to Obamacare, this bill would reduce the deficit by $337 billion over the next 10 years. However, due to tax reductions for the very wealthy, $900 billion dollars would cease to be collected for the same period of time. In addition, the new law would decrease a lot of the bureaucratic mechanisms put in place. This would facilitate administrative matters, and would please free market advocates.

Premiums would initially be more expensive, then cheaper. Yet they would change per the age of the individual, as mentioned. Older insured people would have to pay 5 times more than those of a younger age for the same premium.

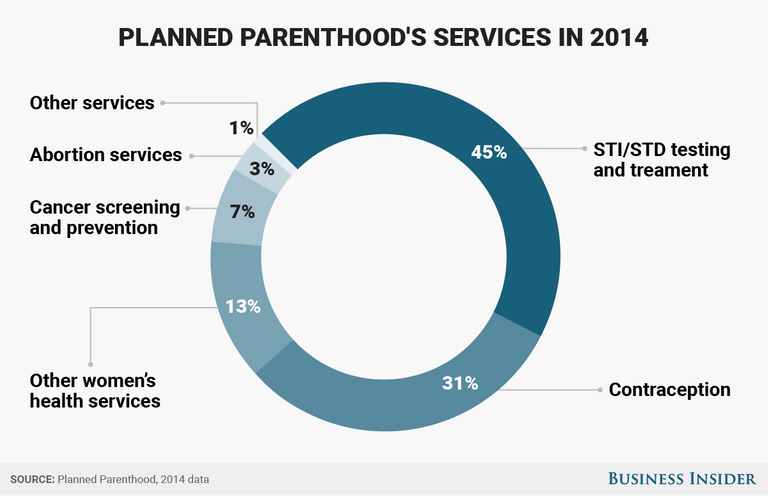

One of the most criticized areas of this plan however, involves its defunding of Planned Parenthood. This would vastly make access to birth control more difficult, which experts claim could increase the number of women seeking abortions, and increase medical expenditures related to these cases.

Other analysts estimate that this law could have other negative effects such as a loss of 924.000 jobs by 2026. Income inequality, with the tax reductions to the highest earners, would worsen quite a bit.

Final verdict

This new bill is seriously tough to defend. It would reduce a lot of the bureaucratic difficulties in the process, and decrease the deficit and net costs associated with Obamacare. It keeps some of the most cherished parts of the previous bill, such as allowing children to stay on their parents’ insurance until 26 years of age.

In terms of healthcare provided though, it’s a disaster. A law created with the intent to improve everyone’s access to healthcare will be changed to benefit the very rich, with the top 6% of the earning population receiving 70% of the benefits of the system. Older and poorer people, as well as those with mental difficulties and chronic diseases will find their lives worsened by this bill. Furthermore, with less tax collection, the deficit covered will likely not be as great as expected.

You should investigate this matter on your own, by all means. But keep in mind that if you are not young, healthy, and wealthy, this bill could worsen your healthcare position. And if you have any elderly, poor people in the family, they will surely be affected.

Time will tell how this situation progresses.

Pretty good read.

Hope you keep this going friend.

Good job.

Thanks good sir! Comments like that make my day!