Hi All,

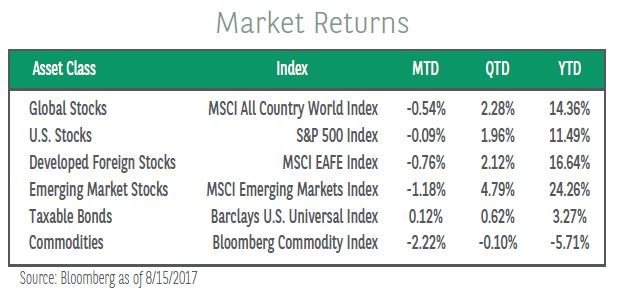

Last Friday marked the close of one of the worst weeks for the U.S. markets this year as tensions over military conflict with North Korea came to a head. While leaders of each country goaded the other in publicized statements, investors fretted over the increased risk of hostilities causing the S&P 500 Index to lose 1.37% for the week. However, the situation seems to have deescalated after North Korea declared they were no longer targeting Guam, a strategic hub for the U.S. in the Pacific; the S&P climbed just over 1% Monday on the news alongside further improvement in company earnings.

As of today, 465 of the companies in the S&P 500 will have reported for the second quarter season, and results continue to delight investors. According to earnings reports aggregated by Bloomberg, average growth in sales rose in the past few weeks to 5.5% and average earnings growth climbed to 9.7%, just shy of the expected double-digit profit growth forecasted by analysts in similar data. But there’s still a chance! There are still forty or so stragglers like Walmart and Costco that will report in the coming weeks, and recent data may suggest the consumer is making a comeback.

Data from the U.S. Census Bureau revealed retail sales in July advanced 0.6%, handedly beating the 0.3% economists expected in a Bloomberg survey, and doubling the pace from last month. The update is a welcomed one as retailers struggle to keep brick-and-mortar stores open amid a trend of sluggish spending from consumers and ecommerce stores rapidly gaining market share. The positive surprise in sales could signal a reversal and may buoy growth due to consumer spending making up a large portion of U.S. GDP. However, they may need to boost outlays by a much larger amount if current economic and market risks persist.

While our team remains cautiously optimistic in regards to the global stock markets, the theme of more attractive opportunities abroad continues. A disconnect between an exceedingly tight labor market and lack of wage pressure in the U.S. may be a cause for concern as investors must patiently wait for inflation to rise. Meanwhile, growth trends outside the U.S. continue to improve. We view the Fed’s unwinding announcement in September and its possible unintended consequences, increased geopolitical risk, slowing profits in the second half of the year, economic growth scares, and potential tightening in China as threats to the advance in global stock markets. Stocks may still have some legs, but investors could be trying to pick up pennies in front of a steam roller.

Last Friday marked the close of one of the worst weeks for the U.S. markets this year as tensions over military conflict with North Korea came to a head. While leaders of each country goaded the other in publicized statements, investors fretted over the increased risk of hostilities causing the S&P 500 Index to lose 1.37% for the week. However, the situation seems to have deescalated after North Korea declared they were no longer targeting Guam, a strategic hub for the U.S. in the Pacific; the S&P climbed just over 1% Monday on the news alongside further improvement in company earnings.

As of today, 465 of the companies in the S&P 500 will have reported for the second quarter season, and results continue to delight investors. According to earnings reports aggregated by Bloomberg, average growth in sales rose in the past few weeks to 5.5% and average earnings growth climbed to 9.7%, just shy of the expected double-digit profit growth forecasted by analysts in similar data. But there’s still a chance! There are still forty or so stragglers like Walmart and Costco that will report in the coming weeks, and recent data may suggest the consumer is making a comeback.

Data from the U.S. Census Bureau revealed retail sales in July advanced 0.6%, handedly beating the 0.3% economists expected in a Bloomberg survey, and doubling the pace from last month. The update is a welcomed one as retailers struggle to keep brick-and-mortar stores open amid a trend of sluggish spending from consumers and ecommerce stores rapidly gaining market share. The positive surprise in sales could signal a reversal and may buoy growth due to consumer spending making up a large portion of U.S. GDP. However, they may need to boost outlays by a much larger amount if current economic and market risks persist.

While our team remains cautiously optimistic in regards to the global stock markets, the theme of more attractive opportunities abroad continues. A disconnect between an exceedingly tight labor market and lack of wage pressure in the U.S. may be a cause for concern as investors must patiently wait for inflation to rise. Meanwhile, growth trends outside the U.S. continue to improve. We view the Fed’s unwinding announcement in September and its possible unintended consequences, increased geopolitical risk, slowing profits in the second half of the year, economic growth scares, and potential tightening in China as threats to the advance in global stock markets. Stocks may still have some legs, but investors could be trying to pick up pennies in front of a steam roller.

Investing involves risk, including the possible loss of principal and fluctuation in value. Economic and market forecasts reflect subjective judgments and assumptions, and unexpected events may occur. Therefore, there can be no assurance that developments will transpire as forecasted. The information in this newsletter is for informational purposes only and is not intended to be investment advice or a recommendation. Nothing in this newsletter should be interpreted to state or imply that past results are an indication of future performance.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Good sharing.

Check my page here https://steemit.com/indonesia/@mahfuddin1/selamat-hari-kemerdekaan-untuk-indonesia-happy-independence-day-for-indonesia