A token is a digital unit created within a specific ecosystem. The token should encourage participants to use the system, which ultimately affects the increase in the value of the token, its turnover, and an increase in the number of ecosystem participants.Tokenomics — a token design process to achieve the ecosystem’s set goals.

The token design process includes:

- Logical elaboration of the tokens flow and game rules in the ecosystem;

- Motivational elaboration of the token (why should participants use it?);

- The mechanism for the appearance of primary tokens (genesis) and the mechanism for the appearance of new tokens in the future (emission policy);

- Token utilization mechanism (if necessary);

- Price policy (how much are the entities in the system).

It is necessary to take into account the design of mechanisms, when developing tokenomic models. It allows you to set the “correct and desired” behavior of the main participants.The simplest example of a mechanism design: a grandmother baked a cake for two grandchildren. It is necessary to cut it so that none of the grandchildren is offended. Most likely, a grandmother without special tools will still cut him not perfectly 50% to 50%. The “fast” grandson will choose a larger piece, and the second grandson will be offended a little. Grandma will be upset. What should they do?We use the design of the mechanisms: the grandmother says to cut the cake to the first grandson, and the second grandson will choose either of the two pieces. As a result, the first grandson will try to cut the pie as evenly as possible, and the second grandson can only choose a better piece. If the first grandson cuts the pie unequally, he will himself be responsible for this misunderstanding. With these rules of the game, no one will be offended by grandmother and will try to behave as rationally and correctly as possible.The main advantage of tokenomic systems is that the design of mechanisms can be programmed in cryptocurrency protocols, in smart contracts and in the stimulating functions of cryptocurrency assets.

As a result, a well-designed token has the following properties:

- Has usefulness in the ecosystem and without it the ecosystem will function less efficiently or will not function in principle;

- It has inflationary resistance, so the issue of tokens is thought out in the system;

- Scalable, tokens can be sent between people quickly and in large volumes;

- Replaceable, unless it is a unique token (non-fungible tokens);

- Accepted by many people, services, artificial systems;

- It has liquidity, tokens are traded on exchanges and p2p sites;

- It has motivational features for use, which are divided into economic incentives (the token holder earns more or saves with it) or managerial incentives (the token holder has the right to vote and is able to influence the ecosystem).

- The token has “rules of the game”, users understand what can be done with this token and what cannot.

Tokenomics can be called an experimental and new field at the intersection of mathematics, statistics, economics (especially macroeconomics and game theory), cryptography, IT, game design and other related disciplines.

Many teams from around the world are struggling with the design of token systems. In the series of works “Tokenomic Arsenal”, I want to consider what principles are used in the design of tokens in existing projects, as well as give abstract examples. By tokenomic technique, I will mean any feature of the token that characterizes it. Each technique will most often be taken apart separately. If it is impossible to separate the techniques, they will be considered together. Each tokenomic technique will have a tokenomic scheme and is described in an extremely accessible way so that it is possible to visually see and parse this particular feature of the token. I would compare the techniques with the individual Lego parts. Each individually is a very simple unit, but during the construction a rather complicated figure can be obtained.

At the current stage of development, it is important for us to understand the essence of the tokenomic techniques that we have accumulated during this time. Yes, they are very simple when considered separately. But first, we understand and describe each element, and then we build something more complex.

As a result, we will have an arsenal of tokenomic techniques, from which we can already form the design of the tokenomic system. In some cases, the description of the tokenomic technique may be inaccurate in order to simplify the understanding of the mechanism.

In the future, I plan to combine tokenomics in order to describe the entire system.

Token Operations:

Token emission (coinbase): a new token appears out of nowhere, tokens are born in the system.

Transfer of tokens: a token from one wallet transfers to another wallet.

Token burning: the token is permanently removed from the system.

Token Freeze: Token loss of liquidity for a specific time. Freezing can be forced, in this case it is more often called a lockup (occurs with private investors, for example). Also, freezing can be voluntary in nature and pursue certain economic and managerial goals. Freezing is carried out through a smart contract or centralized participants in the system.

Unfreezing tokens: the token leaves the defrosting and can freely move in the system. Token infreezing can occur at the user’s call, or it can occur after a certain period of time. There may also be trigger defrost. In this case, a certain event occurs before unfreezing.

Token delegation: temporary token transfer to the validator in the system. At the same time, the validator does not have ownership of tokens, but has pre-registered rights.

Token recall (unbond): The process of returning previously delegated tokens. Most often, this process is accompanied by temporary or other conditions.

Staking: this concept can be understood as freezing tokens and delegating tokens. In this case, the emphasis is on the fact that tokens are given to the use of a third-party entity (validator, smart contract) in order to increase them.

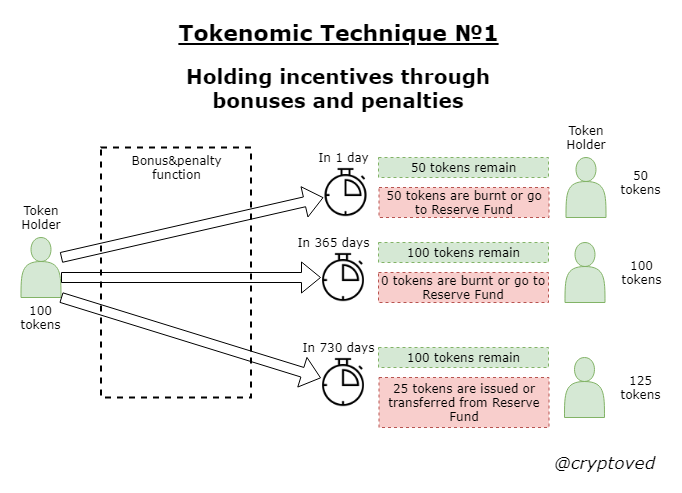

Tokenomic technique №1: holding incentives through bonuses and penalties.

For example, we want to ensure that early investors do not sell tokens to the market. You can come up with a mechanism that for a certain time, the tokens will be unlocked with losses that decrease over time, and then generally turn into bonuses. Releasing tokens on the first day — you lose 50%, while the lost tokens can be burned or sent to the reserve fund of the project. Release tokens in a year — lose 0%. Releasing tokens after 2 years — you will receive a 25% bonus, while the bonus can be obtained through the issue mechanism (new tokens are created) or can be transferred from the reserve fund (that is, no new tokens will be created in this case). Such built-in mechanisms stimulate the desired behavior of token holders and allow the entire system to function in a fairly predictable style. In this case, the path from minus 50% to 25% can be set by a certain function, that is, at any time the token is unlocked, there will be a penalty or bonus.

The main goal: to tune investors to the long-term goals of the project, and not immediate profit. The mechanism cuts off speculators and encourages investors who focus on the fundamental project goals.Scheme of technique:

A similar technique (but only with penalties) was used in the LTO Network project and had the name “Troll Bridge”: https://medium.com/@Price_Steven/a-novel-approach-to-combat-ico-speculation-a2309009ee94

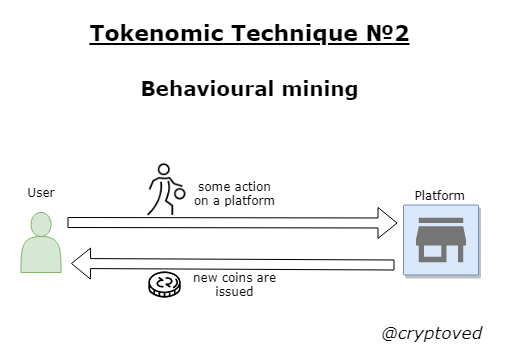

Tokenomic technique №2: behavioural mining.

The mechanism for issuing new tokens may have a different nature. In general, it answers the question — under what conditions and by what rules new tokens appear. One type of emission mechanism is user or behavioral mining. The user performed some action on the platform and received token for it. Let’s look at a few examples:

- The casino user plays in the casino and for a certain turnover receives the token of this casino. For example, you need to make a turnover of 10 ETH and then the user will receive a new casino token;

- The buyer makes a purchase in the online store and, based on the volume, receives tokens of the online store. This is very similar to the loyalty system, when points are generated when buying in the online store, which the user can spend on subsequent purchases. The only difference is that now this token can have other properties. Perhaps he is endowed with a dividend function, and in this case, the buyer of the online store to some extent becomes a co-owner of the online store and will receive a fraction of all future profits;

- In a decentralized taxi application, the driver and passenger can both receive system tokens from each trip, and these tokens can have their own purpose.

The main goal: the platform rewards those who use the services of the platform. In my opinion, this is a fairly fair mechanism for rewarding loyal users in order to keep them on the platform for a long period of time.

Scheme of technique:

A similar technique is often used in gambling projects: Dice, Rake, Live — Dapps in the Wink ecosystem. Also, a similar mechanism is used in Gojoy — a service of joint and wholesale purchases.

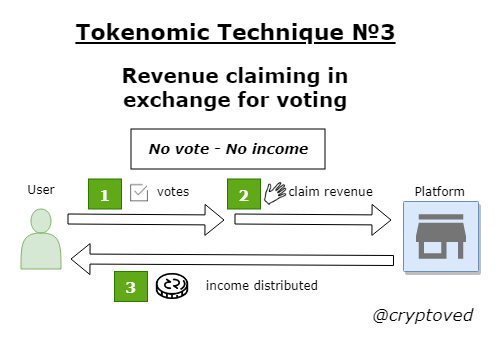

Tokenomic Technique №3: revenue claiming in exchange for voting.

Often, DAO systems introduce voting for token holders. “Percentage of turnout” here suffers very much, as in life. The active majority votes, which in some cases is about 2–5%. If we want to raise the “turnout percentage”, then the voting should be built in before the process of claiming (requesting) the system’s income, if any. Also, this mechanism should be invested in a convenient user interface, and not manual interaction with a smart contract.At the same time, income can have a different nature: share premium (tokens are created from scratch), redistributive income (tokens are paid from platform profit), income based on a certain job and other types.

The main goal: to increase the percentage of voters in the system by introducing economic incentives for voting. To some extent, this mechanism can also be used for the legal shell of the dividend system, which becomes not purely a dividend, since before receiving income, the tokenholder needs to do some more management work.

Scheme of technique:

A similar technique is used in the Dlive streaming platform: https://help.dlive.tv/en-us/article/locked-points-mhl19t/

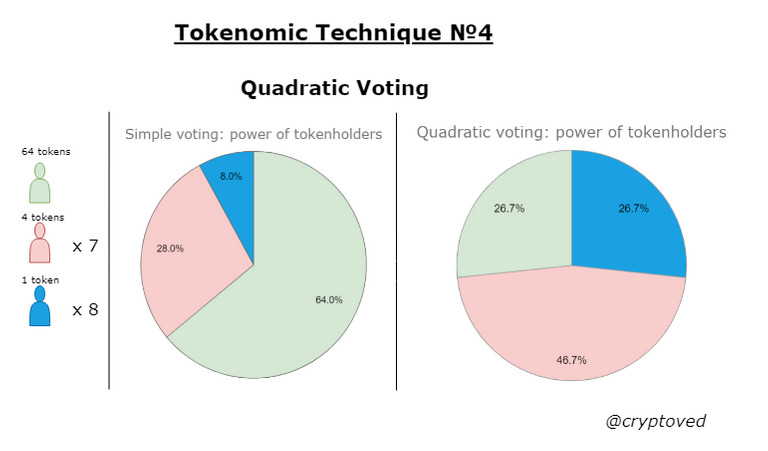

Tokenomic Technique №4: Quadratic Voting.

Quadratic voting is a type of voting in which the number of votes of a participant is equal to the square root of the amount paid by him or the tokens available in the hands of one participant (according to the formula “for X monetary units / tokens you get the square root of X votes”). This type of voting allows to reduce the superiority of wealthy participants in the system and to obtain more even voting results.

For example, the system has a majority token holder with 64 tokens, there are 7 people with 4 tokens each and there are 8 more people, each with one token. There are 100 tokens in the system. If we had a regular vote, then the majority token holder would always win (he has 64% of the vote) and the rest would not even make sense to vote.

With a quadratic vote, everything becomes more interesting. Our rich token holder gets 8 votes, 7 average holders have 2 votes each (a total of 14) and 8 more votes from the smallest token holders. The managerial strength of the rich player is smoothed out, now he has only 26.67% of the total number of votes (8/30). Smaller tokenholders have an incentive to vote. The system is becoming more balanced, now every vote is important. At the same time, a rich token holder can redistribute its tokens among different affiliated accounts and thereby gain more votes in the system. Most likely, in this case, a procedure for identifying users is necessary or “wallets” created before a certain date have the right to vote. Of course, in each case, it is necessary to carefully consider the mechanisms of protection against the unfair game of a rich token holder.

The main goal: quadratic voting eliminates the hegemony of the ruling elite and redistributes managerial functions more evenly. Such a system does not allow slide into authoritarianism and total power of the main token holders.

Scheme of technique:

The concept of quadratic voting is popular with followers of radical markets and developers of DAO in the Ethereum ecosystem.

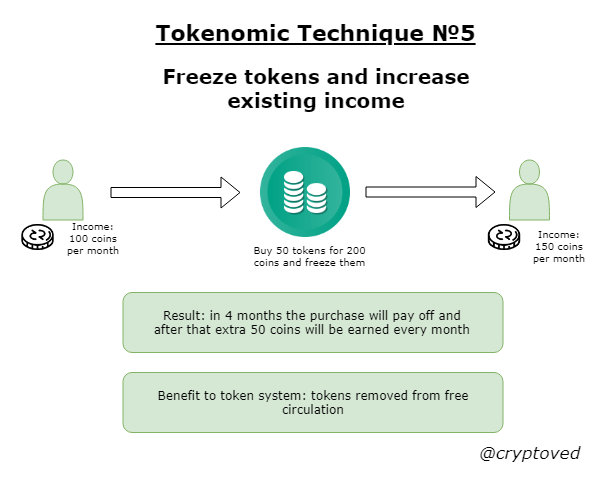

Tokenomic Technique №5: freeze tokens and increase existing income.

A person already has income in some system. He can increase it if he buys and freezes certain tokens. It is important not to confuse this technique with dividends: until the purchase and freezing of tokens, a person does not receive dividends. In our case, a person already has an income without tokens, but he can increase it by buying tokens.Let’s consider hypothetical and real examples:

- Binance Exchange pays 20% of the referrals you attracted. This percentage can be doubled immediately if there are 500 BNB tokens in the account. Thus, withholding tokens increases existing revenues (in the future).

- Let’s say we work for some cryptocurrency structure and get 10 ETH monthly. We can start to receive 15 ETH for the same work, but only on condition that we buy ABC tokens in the amount of 1000 pieces and freeze them on a smart contract.

The main goal: this technique allows you to reduce the number of tokens in free circulation on the one hand and at the same time increases the loyalty of current beneficiaries.

Scheme of technique:

Tokenomic technique is used in the referral program of the Binance exchange. It played an important role in the success of this exchange.

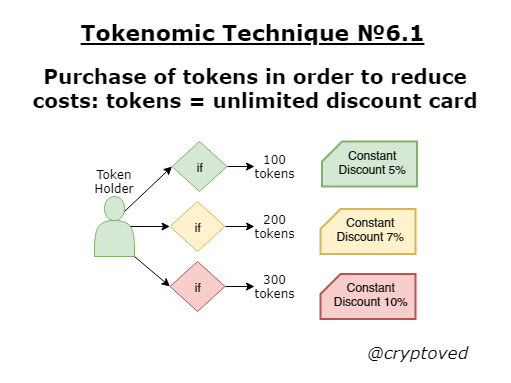

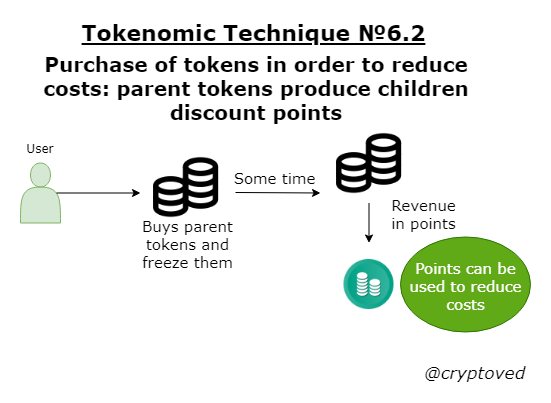

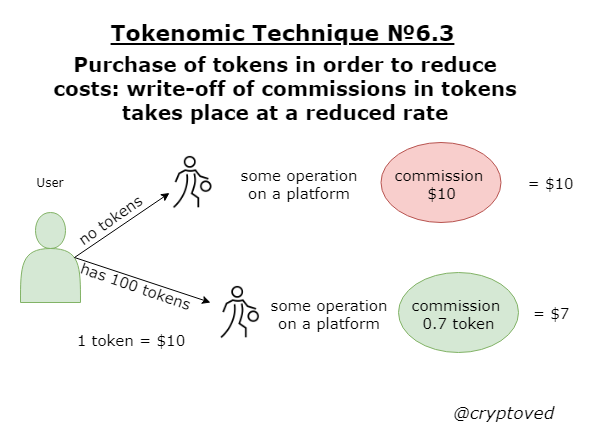

Tokenomic Technique №6: purchase of tokens in order to reduce costs.

The user incurs certain costs in the system, but he can reduce them by buying tokens. It would seem that this is a fairly simple mechanism and in the public sense it can be compared with a discount card. The freedom of tokenomic functionality allows us to use this technique in more diverse forms.Consider examples of cost reduction. In this technique, for each case, we will also draw up our own scheme to more clearly distinguish one variation from another.

The main goal: to create an economic incentive for the purchase of tokens in order to reduce user costs in the system. The mechanism allows you to remove tokens from circulation or to launch an active circulation of tokens.

6.1. Tokens = unlimited discount card. While we keep tokens in a certain amount — our discount is valid. At the same time, an interval discount system can be created when one number of tokens entitles you to a 5% discount and another 7%. Reception allows for a long period of time to remove tokens from free circulation. This case is used by many types of real business.

6.2. Parent tokens produce children discount tokens.

This is a more complicated case, here we have two types of tokens. Parent tokens can be bought and frozen and they will periodically serve as a trigger for the issue of discount tokens. For example, we froze 100 parent tokens. At the end of the month, we accrued profitability, but it happened in separate tokens that can already be spent on reducing the purchase amount. In the system, we will call such tokens points. The point rate can be tied to a stable coin or other calculation currency in the system. Something similar can be observed in the Tron’s ecosystem, when the long holding of a certain number of TRX makes transactions free of charge due to the accumulated energy.

6.3. Write-off of commissions in tokens takes place at a reduced rate.

Here, the simplest example is the commission mechanism on the Binance exchange with BNB tokens. For example, you trade 10 bitcoins and a commission of 0.01 BTC should be debited from you, after that you will have 9.99 BTC left. But you can reduce the commission level by 30% if the commission is written off in BNB tokens. In this case, the system will automatically transfer 0.01 BTC at the current rate to BNB, multiply the amount received by 0.7 and withdraw this number of BNB from you. In this case, 10 BTC will remain 10 BTC. This mechanism allows creating an economic demand for tokens (users will buy them in order to save on commissions) and launch an active token circulation.

Tokenomic technique №7: holding tokens in order to participate in IEO.

A model that gained fame in 2019. The user holds exchange tokens for a certain time and then can participate in crowdinvesting of a new project.The exchange most often requires holding exchange tokens for a certain period until IEO (in some cases, there is no such obligation), and then accepts investments in the exchange tokens themselves and sometimes in another cryptocurrencies. Acceptance in another cryptocurrency is beneficial in that in the future it does not affect the price of the exchange token itself. After a certain time, the project will begin to sell the cryptocurrency collected during IEO. And if these are exchange tokens, this will create pressure on the price. In my opinion, the most compromise and equilibrium scheme is the requirement to hold exchange tokens (we remove exchange tokens from free circulation) and accept IEO funds in a more popular currency (as a result, this does not put negative pressure on the exchange rate in the future). Such model is more stable in the long-term period of time, does not create serious pump and dump patterns when users and projects have a high demand for a short period of time, or vice versa, an offer for exchange tokens.

The main goal: listing on the exchange new projects, which, as a rule, are of higher quality, in contrast to stand-alone ICOs. With this model, the scoring of projects is carried out by the exchange itself, which ultimately reduces the level of low-quality and fraudulent products, systems and platforms. The project itself receives attention from users of the exchange and the entire cryptocurrency community. Investors in this scheme invest in more reliable projects and in some cases multiply them in a fairly short period of time. The exchange, in turn, encourages token holders to hold their tokens, thereby reducing the circulation of freely circulating tokens.

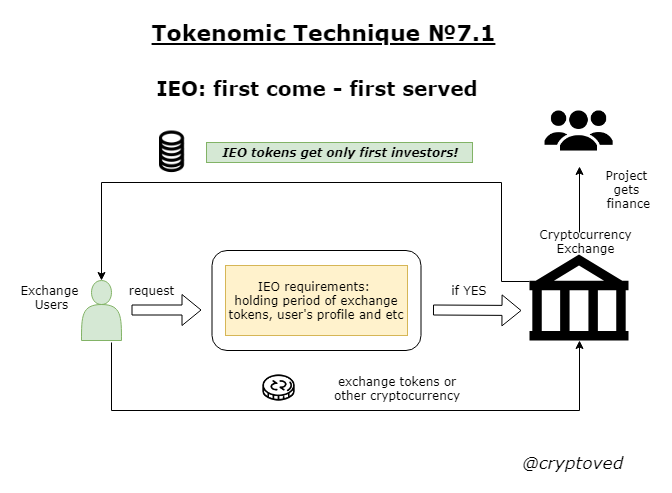

7.1. Investors invest in IEO according to the principle: first come — first served.

Under this scheme, investors invest in a new project on the basis of urgency. Whoever managed to invest first got tokens. Sometimes such IEOs close in a few seconds, and demand exceeds supply by several times.

This scheme was used in the first IEOs on Binance, on Bittrex, Huobi and other cryptocurrency exchanges.

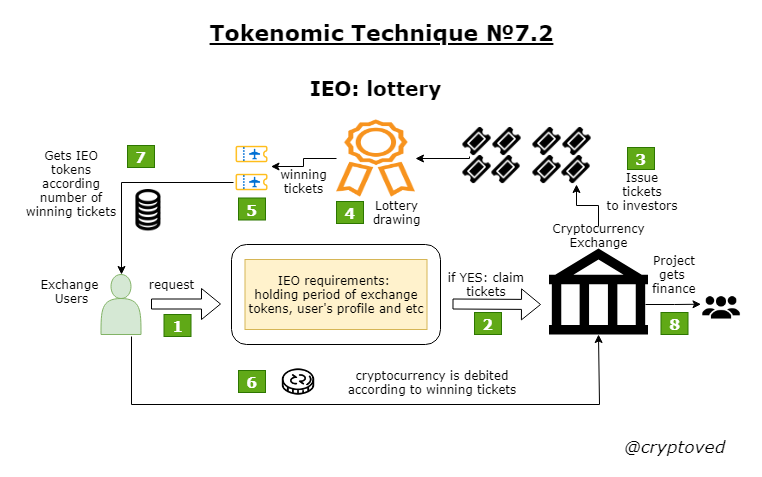

7.2. Investors invest in lottery-based IEOs.

The FCFS scheme had its drawbacks: there were many dissatisfied investors who did not manage to participate in IEO. Also, people began to abuse bots to be the first. As a result, an ordinary investor had practically zero chances to participate in IEO according to FCFS scheme. The lottery model was replaced, where each investor already had the same chance to participate in IEO. Depending on the number of holding tokens, lottery tickets are issued for a certain period. The number of tokens can be average for the period or minimum for the entire period. The lottery winners are charged a certain number of exchange tokens, and in return they receive IEO tokens of the project.

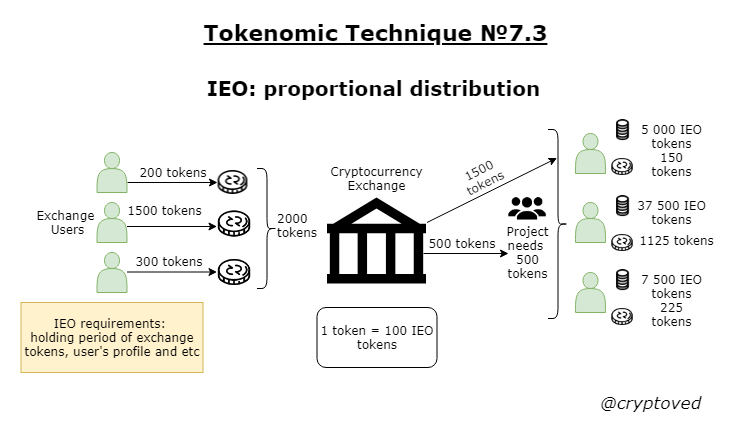

7.3. Proportional distribution of IEO tokens.

The lottery scheme also has its drawbacks: not everyone is lucky, especially if the investor has few lottery tickets. Some exchanges have begun to apply a proportional token distribution model, often also called the Fusion model. With this scheme, the amount of raising funds is announced, investors make bids or even actually transfer funds to IEO. If the amount of necessary funds was X conventional units, and investors sent 5X conventional units, then each investor will enter only 20% of the planned capital. With such a model, it is important to predict the demand of investors for the project and take into account that only a part of the capital will enter you. Also in this model there may be various variations: for example, those who submitted the application before everyone else may have a raising coefficient. Or the scheme may have a limit on top, for example, 10X conventional units. Also, different coefficients may depend on the retention period of exchange tokens. The basic idea always remains the same: the investor receives the project tokens only for a part of the capital, depending on the demand of other investors.

In some cases, the exchange may combine IEO schemes. For example, at the first stage, arrange the FCFS model, and at the second stage, make a proportional distribution of tokens. In this case, each stage may have different conditions (up to token prices). A combination of schemes was observed at the exchanges Okex, Huobi.

This is the first part of the tokenomic arsenal, where only 7 tokenomic techniques are considered. In the future I plan to continue a series of notes and make out other techniques and systems.

Feedback: @onlypreico_bot in Telegram

Telegram channel: https://t.me/cryptovedinvest

I will be glad to receive a description of interesting tokenomic techniques. If there are inaccuracies in the text or you have comments, then welcome too.

Are you developing a cryptocurrency project? I will consider the possibility of joining the team in terms of developing tokenomics and a business model (schemes, tables, descriptive part).

You can support my work:

BTC: 3Qg1N1MFCbewGHqcUkyR289dvoMJpNkJEK

LTC: MStocnUxWHg8xs87FJZVfvAABzn9cmrrqn

ETH: 0x8484e207E84783F65d584254A44C8d3814437d5a

Thanks!

Congratulations @cryptoved! You have completed the following achievement on the Steem blockchain and have been rewarded with new badge(s) :

You can view your badges on your Steem Board and compare to others on the Steem Ranking

If you no longer want to receive notifications, reply to this comment with the word

STOPTo support your work, I also upvoted your post!

Do not miss the last post from @steemitboard:

Vote for @Steemitboard as a witness to get one more award and increased upvotes!